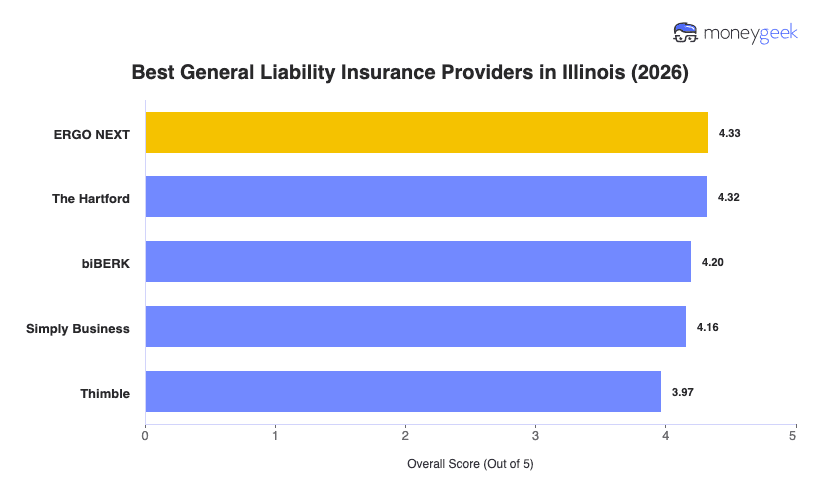

MoneyGeek's best general liability insurance companies in Illinois are ranked on pricing stability, claims responsiveness and coverage fit for small businesses. A Naperville contractor, a Chicago food truck operator and a Bloomington retail shop each carry different risk profiles. These five carriers ranked highest across all three factors:

- ERGO NEXT: Best Overall, Best for Customer-Facing Businesses

- The Hartford: Best Cheap General Liability Insurance

- biBERK: Best for Service-Based Businesses with Straightforward GL Needs

- Simply Business: Best for Multi-Carrier Quotes

- Thimble: Best for Flexible Coverage Terms