The Hartford is the best workers' comp insurance in Minnesota, averaging $91 per employee per month and ranking first for both overall score and affordability among the 10 providers MoneyGeek reviewed. ERGO NEXT ties it on price at an average rate of $91 and ranks second overall, with the top customer experience score in the group. Both pull well ahead of the rest of the field. The next cheapest option, Thimble, averages $97 per month, while the most expensive, Chubb, averages $148.

Best Workers' Comp Insurance in Minnesota (2026)

With rates as low as $9 monthly, The Hartford, ERGO NEXT and Coverdash offer the cheapest and best workers' comp insurance in Minnesota.

Get matched to top Minnesota workers' comp insurance providers and find your ideal coverage.

Select state

Updated: June 26, 2026

Advertising & Editorial Disclosure

Best Minnesota Workers' Comp Insurance: Fast Answers

The Hartford leads Minnesota workers' comp providers with the top MoneyGeek score. Both The Hartford and ERGO NEXT average $91 per employee monthly, tying as the cheapest providers in the state.

- The Hartford: $91 a month

- ERGO NEXT: $91 a month

- Thimble: $97 a month

- biBERK: $101 a month

- Coverdash: $103 a month

Minnesota requires workers' comp coverage for all employers with at least one employee. Non-compliance is a misdemeanor criminal violation (not merely a civil penalty) and exposes employers to personal liability for all injury costs. The Minnesota Department of Labor and Industry administers enforcement.

Minnesota's state average is approximately $112 per employee monthly, above the $74 national average. Beauty, Body and Wellness Services and Financial Services are among the most affordable industries, with state averages around $15 a month. Transportation and Logistics ($339 a month) and Construction ($311 a month) are the most expensive in the state.

Minnesota employers get workers' comp coverage through private insurers in a competitive market. The Minnesota Workers' Compensation Assigned Risk Plan (MWCARP) provides coverage for employers who can't obtain voluntary market coverage.

- Medical expenses: Covers all reasonable and necessary medical treatment; the Minnesota Department of Labor and Industry administers the fee schedule.

- Wage loss benefits: Pays temporary total disability at 66⅔% of the employee's average weekly wage (verify 2026 maximum against the Minnesota Department of Labor and Industry).

- Vocational rehabilitation: Minnesota's mandatory rehabilitation consultation program requires carriers to provide rehab support to qualifying injured workers within a specified timeframe.

- Death benefits: Pays burial expenses and compensation to qualifying dependents based on the deceased worker's average weekly wage.

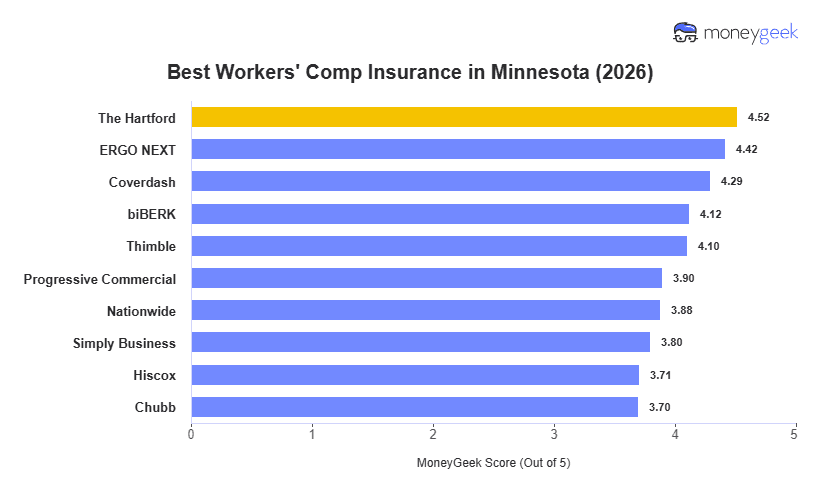

Best Workers' Comp Insurance Companies in Minnesota

| The Hartford | 4.52 | 90.91 | 3 | 3 |

| ERGO NEXT | 4.42 | 90.76 | 1 | 6 |

| Coverdash | 4.29 | 102.98 | 5 | 1 |

| biBERK | 4.12 | 101.09 | 8 | 8 |

| Thimble | 4.10 | 97.42 | 8 | 9 |

| Progressive Commercial | 3.90 | 111.35 | 8 | 7 |

| Nationwide | 3.88 | 114.34 | 6 | 5 |

| Simply Business | 3.80 | 131.85 | 2 | 2 |

| Hiscox | 3.71 | 126.07 | 6 | 10 |

| Chubb | 3.70 | 148.37 | 3 | 4 |

How Did We Determine These Rates and Rankings?

These rates are estimates based on MoneyGeek's analysis of small businesses with one to four employees across 408 major industries. Actual rates vary based on your business location, industry risk factors, claims history, coverage limits and individual insurer underwriting criteria. Contact insurers directly for personalized quotes.

The Hartford

Best Workers' Comp Insurance in Minnesota

MoneyGeek Rating

4.5/ 5

4.1/5Affordability Score

4.2/5Customer Experience Score

4.3/5Coverage Score

Average Monthly Cost

$91Claims Processing Score

4.1/5Policy Management Score

4/5Buying Process Score

4/5

ERGO NEXT

Best Minnesota Workers' Comp Insurance: Runner-Up

MoneyGeek Rating

4.4/ 5

4.1/5Affordability Score

4.5/5Customer Experience Score

3.8/5Coverage Score

Average Monthly Cost

$91Claims Processing Score

4/5Policy Management Score

4.1/5Buying Process Score

4.4/5

LEARN MORE ABOUT MINNESOTA BUSINESS INSURANCE

Cheapest Workers' Comp Insurance in Minnesota by Industry

The Hartford is the cheapest workers' compensation provider in more Minnesota industries than any other provider in our analysis, leading in 13 of 25 categories. Its strongest price advantage is in low-hazard work, including financial services ($9 a month), consulting ($15 a month) and marketing ($13 a month).

ERGO NEXT leads where physical risk is highest, including Construction ($217 a month) and Agriculture ($152 a month). Two providers appear in just one category each: Progressive Commercial for Transportation and Logistics, and Coverdash for Fitness Services, both worth comparing if your business falls in those categories.

| Agriculture & Natural Resources | ERGO NEXT | $152 | $1,824 |

| Arts, Media & Entertainment | Thimble | $88 | $1,056 |

| Beauty, Body & Wellness Services | The Hartford | $12 | $144 |

| Childcare Services | biBERK | $31 | $372 |

| Cleaning Services | The Hartford | $103 | $1,236 |

| Construction & Contracting | ERGO NEXT | $217 | $2,604 |

| Consulting Services | The Hartford | $15 | $180 |

| Education | ERGO NEXT | $60 | $720 |

| Financial Services | The Hartford | $9 | $108 |

| Fitness Services | Coverdash | $59 | $708 |

| Food & Beverage | ERGO NEXT | $39 | $468 |

| Healthcare & Medical | The Hartford | $38 | $456 |

| Hospitality, Travel & Tourism | The Hartford | $36 | $432 |

| Manufacturing | The Hartford | $126 | $1,512 |

| Marketing & Communications | The Hartford | $13 | $156 |

| Nonprofit & Associations | The Hartford | $48 | $576 |

| Other Professional Services | The Hartford | $19 | $228 |

| Pet Care Services | ERGO NEXT | $58 | $696 |

| Real Estate & Property Services | The Hartford | $16 | $192 |

| Recreation & Sports | ERGO NEXT | $102 | $1,224 |

| Repair & Maintenance | ERGO NEXT | $67 | $804 |

| Retail & Product Rental | The Hartford | $44 | $528 |

| Tech/IT | The Hartford | $29 | $348 |

| Transportation & Logistics | Progressive Commercial | $272 | $3,264 |

| Wholesale & Distribution | biBERK | $173 | $2,076 |

Average Workers' Comp Insurance Cost in Minnesota by Industry

The average cost of workers' comp insurance in Minnesota is $112 per employee monthly, but rates vary widely by industry. The spread across Minnesota industries runs from $15 monthly for financial services to $339 for transportation and logistics. That's a 23x difference that reflects how dramatically physical risk affects workers' comp rates.

| Beauty, Body & Wellness Services | $15 | $180 |

| Financial Services | $15 | $180 |

| Marketing & Communications | $16 | $192 |

| Consulting Services | $22 | $264 |

| Real Estate & Property Services | $24 | $288 |

| Other Professional Services | $25 | $300 |

| Childcare Services | $41 | $492 |

| Food & Beverage | $46 | $552 |

| Tech/IT | $46 | $552 |

| Hospitality, Travel & Tourism | $47 | $564 |

| Healthcare & Medical | $56 | $672 |

| Retail & Product Rental | $61 | $732 |

| Nonprofit & Associations | $64 | $768 |

| Pet Care Services | $71 | $852 |

| Fitness Services | $72 | $864 |

| Education | $73 | $876 |

| Repair & Maintenance | $82 | $984 |

| Arts, Media & Entertainment | $102 | $1,224 |

| Recreation & Sports | $128 | $1,536 |

| Cleaning Services | $133 | $1,596 |

| Manufacturing | $158 | $1,896 |

| Agriculture & Natural Resources | $184 | $2,208 |

| Wholesale & Distribution | $203 | $2,436 |

| Construction & Contracting | $311 | $3,732 |

| Transportation & Logistics | $339 | $4,068 |

Minnesota Workers' Comp Insurance Cost Factors

These cost factors affect workers' compensation insurance rates in Minnesota:

How Much Workers' Comp Insurance Do I Need in Minnesota?

Minnesota law requires all employers to purchase workers' compensation insurance or become self-insured, regardless of business size. You need the required workers' compensation coverage even with just one part-time employee.

Your policy must provide unlimited medical treatment for work-related injuries and wage loss benefits paying two-thirds of your employee's average weekly wage. Coverage amounts scale based on your payroll and industry classification code. Skipping coverage can cost you up to $1,000 per employee per week in fines. If an employee gets injured while you're uninsured, you'll reimburse the state's Special Compensation Fund plus a 65% penalty.

Minnesota Workers' Comp Insurance Exemptions

You're required to have coverage in Minnesota, but some business categories are exempt from workers' comp requirements:

- Sole proprietors who are self-employed can exclude themselves and immediate family members (spouse, parents, children) working in the business from coverage requirements.

- Business partners enjoy the same exemption for themselves and their spouse, parents and children employed by the partnership.

- Corporate officers and LLC managers who own at least 25% of a closely held business can opt out of coverage. Your business qualifies as "closely held" if it has 10 or fewer shareholders (or members for LLCs) with less than 22,880 payroll hours annually. This exemption extends to your spouse, parents and children working in the company.

- Extended family members of qualifying owners can also be excluded. This includes relatives within the third degree of kinship: uncles, nieces, siblings and grandchildren. You'll need to file a written election with the Minnesota Department of Labor and Industry.

- Family farm workers employed by qualifying family farms don't need coverage. This exemption extends to the farmer's spouse, parents and children working in the operation, along with executive officers of family farm corporations.

- Household employees earning less than $1,000 in a three-month period from a single household don't require coverage. This includes domestic workers, repairers, groundskeepers and maintenance workers in private homes.

- Casual employees performing occasional labor outside your normal business operations are exempt from coverage requirements.

- Independent contractors who work for multiple clients, set their own schedules, provide their own tools and control how they complete their work don't need workers' comp coverage. The key distinction is that you can't control when, where or how they do their job.

- Small nonprofit organizations paying less than $1,000 in total annual wages can skip coverage. Officers or members of veterans' organizations whose only employment relationship involves attending meetings or conventions are also exempt unless the organization chooses to provide coverage.

- Federal program volunteers like AmeriCorps or Senior Corps members fall outside state workers' compensation requirements since they're covered under federal programs.

How to Get the Best Workers' Comp Insurance in Minnesota

Find out how to get workers' comp insurance with the right provider at the best price.

- 1Determine if you need workers' comp coverage in Minnesota

Verify whether workers' comp exemptions apply to your business structure or employee types before assuming you're covered. A sole proprietor graphic designer doesn't need coverage, but hiring one employee changes that requirement. Minnesota classifies workers differently than most states, so people you consider independent contractors may legally qualify as employees who require coverage.

- 2Gather your business information

Gather your employee count, annual payroll and classification codes for accurate quotes. Minnesota uses the National Council on Compensation Insurance system with industry-specific codes that determine your rates.

Accurate payroll figures and classification codes are the foundation of a correct workers' comp quote in Minnesota. Estimating either number or using the wrong classification code can trigger audit penalties or leave you with coverage gaps at claims time. Restaurants and construction businesses face extra scrutiny because Minnesota applies different rates for tipped employees and seasonal workers. - 3Request workers' comp quotes from multiple carriers

Pull quotes from at least three insurers when comparing business insurance costs. Minnesota has no state insurance fund, so coverage comes through private carriers or the assigned risk pool for businesses that can't secure voluntary market coverage. Add the assigned risk pool to your list only if private carriers decline your application, since pool rates run 20% to 30% above voluntary market pricing. Rates vary widely by industry and loss history, so target insurers that specialize in your field rather than defaulting to household names.

- 4Research providers with industry experience

Low premiums matter, but the right insurer also needs to understand your specific business risks. Browse affordable business insurance rates as a starting point, then narrow to carriers with relevant industry experience. Warehousing operations do better with carriers that know material handling injuries and OSHA standards than with general commercial providers.

- 5Evaluate your top provider options

Four criteria help identify the best insurance for your business in Minnesota:

- Check claim processing speed, service quality and complaint records filed with the Minnesota Department of Commerce.

- Confirm the insurer offers managed care networks that control medical costs and coordinate treatment for injured workers.

- Ask about its experience navigating Minnesota's workers' compensation court and its success rate with disputed claims.

- Look for safety training resources, return-to-work programs and workplace assessments built for Minnesota employers.

- 6Review and purchase your workers' compensation policy

Review policy terms with attention to coverage limits, exclusions and renewal conditions specific to Minnesota regulations. Match payment structures to your cash flow. Pay-as-you-go workers' comp suits Minnesota businesses with variable payrolls by tying premiums to actual wages rather than annual estimates. Ask each insurer about premium discounts for safety programs or claim-free periods before signing.

- 7Reassess before annual renewal

Before your policy renews, audit three numbers: employee count, filed claims and your experience modification rate. Businesses change between renewal cycles. Hiring staff, expanding services or relocating all affect your risk profile and premium. Tell your insurer about any changes before renewal to avoid overpaying or carrying coverage gaps. Minnesota rates adjust based on statewide trends, so premiums can rise even without claims.

Best Minnesota Workers' Compensation Insurance: Bottom Line

The Hartford, ERGO NEXT and Coverdash lead Minnesota's workers' comp rankings. Businesses should research each company's service quality, maximize discounts and select coverage that fits their budget.

MoneyGeek analyzed workers' comp insurance rates and provider performance across Minnesota using small business profiles with one to four employees spanning 408 major industries. Companies earn up to five points in each category in our scoring system. We then use a weighted average of these category scores to calculate a MoneyGeek score out of five.

- Affordability (55%): Based on average payroll for the most common employee code per industry and state classification, priced per employee for a one to four employee business.

- Customer Experience (35%): Evaluates buying (20%), which covers quote access, pricing accuracy and sales support; policy management (30%), which covers payroll reporting, audits, billing and loss control; and claims (50%), which covers FNOL speed, adjuster support, medical access, wage replacement and dispute handling.

- Coverage Options (10%): Assesses coverage completeness (35%), including employers' liability and wage and medical reimbursement; policy flexibility and endorsements (25%); eligibility, state and industry breadth (20%); and policy terms, limits and exclusions (20%).

About Connor Bolton

Connor Bolton is Senior SEO and Content Manager at MoneyGeek, where he leads the business and pet insurance editorial teams. He sets the research framework, data standards and content structure for his team. All content goes through his accuracy review before publication. Connor also writes in-depth guides and has spent more than four years covering insurance products across personal, commercial and specialty lines.

The research infrastructure Connor built covers auto, home, renters, life, health, business and pet insurance across pricing analysis, carrier research, customer experience and coverage evaluation. It includes over 6 million data points for business insurance across 408 industry areas, all 50 states and 16 vehicle types. The pet insurance side covers over 5 million profiles across 18 major providers, 100+ breeds and ages up to 20 years. Connor’s insurance research and his team's work have been cited by the U.S. Chamber of Commerce, Allstate, Liberty Mutual, CBS News, Forbes and LegalZoom.

Connor also talks with underwriters and carrier liaisons at Ethos, The Hartford, ERGO NEXT, Nationwide and State Farm, and monitors business and pet owner communities on Reddit. Those sources shape how his team evaluates carriers, structures rate analysis and writes content for real pet owners.

Questions about MoneyGeek's business or pet insurance content? Reach him at connor@moneygeek.com or on LinkedIn.

Sources

- Minnesota Department of Labor and Industry. "Fines and Penalties for Employers' Failure to Insure." Accessed August 8, 2026.

- Minnesota Department of Labor and Industry. "Independent Contractor or Employee." Accessed August 8, 2026.

- Minnesota Department of Labor and Industry. "Rate Information, Statewide Average Weekly Wage (SAWW)." Accessed August 8, 2026.

- Minnesota Department of Labor and Industry. "Results of Special Compensation Fund Assessment." Accessed August 8, 2026.

- Minnesota Department of Labor and Industry. "Waiting Period After Injury." Accessed August 8, 2026.

- Minnesota Department of Labor and Industry. "Wage-Loss and Monetary Benefits." Accessed August 8, 2026.

- Minnesota Department of Revenue. "Commerce Approves Decrease in Rates for Businesses Buying Workers' Compensation Insurance Through State Program." Accessed August 8, 2026.

- Minnesota Legislature. "176.181 Insurance." Accessed August 8, 2026.

- Minnesota Workers' Compensation Insurers Association. "Agent FAQs." Accessed August 8, 2026.

- Minnesota Workers' Compensation Insurers Association. "Minnesota Contractors Premium Adjustment Program." Accessed August 8, 2026.

- Workers Compensation Research Institute. "Workers Compensation Premium Credits for Construction Contractors." Accessed August 8, 2026.