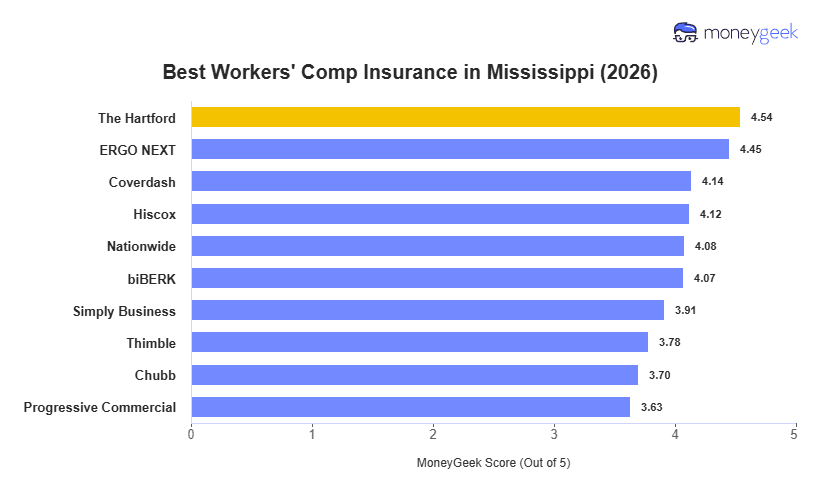

The Hartford leads Mississippi's rankings for the best workers' comp insurance, combining the state's top affordability rank with strong claims performance. ERGO NEXT ranks second, matching The Hartford's average monthly rate and holding the highest customer experience score in the state. Both providers average $57 per employee monthly, Mississippi's lowest rate among all ranked workers' comp insurance providers we reviewed.

The $38 spread from the cheapest providers to the most expensive ranked provider (Chubb at $95 a month) gives Mississippi employers a meaningful range to shop. Professional-sector businesses capture the most value from that gap, where pricing varies more widely.