The Hartford is the best workers' comp insurance in Maine, averaging $81 per employee per month, the lowest rate among the 10 providers MoneyGeek reviewed. It ranks first for affordability and third for both customer experience and coverage. Second-ranked Coverdash costs $89 per month and leads the group in coverage quality, a good alternative for businesses that prioritize plan depth over price.

Best Workers' Comp Insurance in Maine (2026)

With rates as low as $9 per month, The Hartford and Coverdash have the best workers' comp insurance in Maine.

Get matched to top Maine workers' comp insurance providers and find your ideal coverage.

Select state

Updated: May 29, 2026

Advertising & Editorial Disclosure

Best Maine Workers' Comp Insurance: Fast Answers

What are the best and cheapest workers' comp insurance providers in Maine?

The Hartford is the best workers' comp provider in Maine and also has the cheapest average monthly rate:

- The Hartford: $81/month

- Coverdash: $89/month

- Thimble: $90/month

- Nationwide: $101/month

- Hiscox: $101/month

Is workers' comp insurance required in Maine?

Maine requires workers' comp coverage for employers with one or more employees. The Maine Workers Compensation Board serves as the oversight body for the state's workers' comp system. Employers who fail to comply incur civil fines, stop-work orders and personal liability for all injury costs sustained by uninsured workers.

How much does workers' comp insurance cost in Maine?

Maine's state average is $99 per employee per month, $15 above the $74 national average. The cheapest industry in Maine is Beauty, Body & Wellness Services at $15/month, while Transportation & Logistics averages $300/month.

How do you get workers' comp insurance in Maine?

Maine's market includes both private carriers and Maine Employers Mutual Insurance Company (MEMIC), which operates as a competitive state fund alongside private insurers. Employers who can't obtain coverage in the voluntary market can access the NCCI-administered assigned risk pool as a backstop. Including MEMIC in your comparison is especially important for Maine employers, as it holds a primary position in the state market.

What does Maine workers' comp insurance cover?

Maine workers' comp insurance covers the following:

- Medical expenses: Covers all necessary medical treatment for work-related injuries; the Maine Workers Compensation Board administers the fee schedule.

- Wage loss benefits: Pays temporary total disability at 80% of the employee's average weekly wage (verify 2026 maximum weekly benefit against the Maine Workers Compensation Board).

- Vocational rehabilitation: Provides retraining and placement services for workers unable to return to their pre-injury occupation.

- Death benefits: Pays burial expenses and compensation to qualifying dependents based on the deceased's average weekly wage.

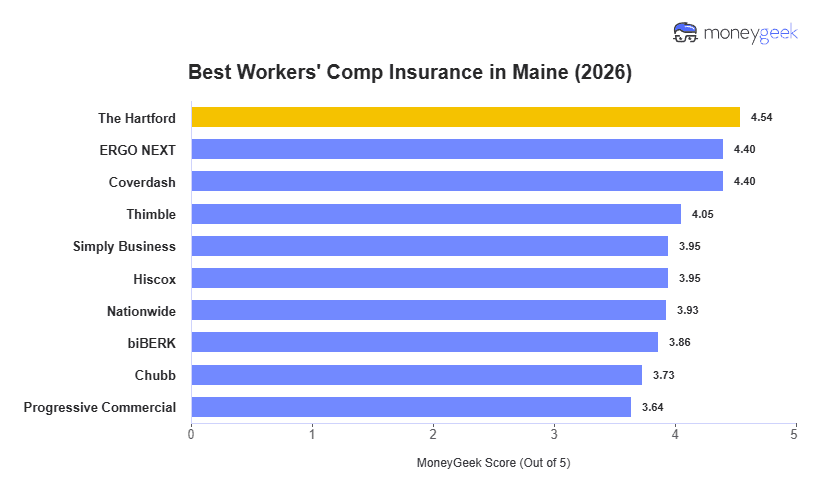

Best Workers' Comp Insurance Companies in Maine

| The Hartford | 4.54 | $81 | 3 | 3 |

| ERGO NEXT | 4.40 | $83 | 1 | 6 |

| Coverdash | 4.40 | $89 | 5 | 1 |

| Thimble | 4.05 | $90 | 8 | 9 |

| Simply Business | 3.95 | $107 | 2 | 2 |

| Hiscox | 3.95 | $101 | 6 | 10 |

| Nationwide | 3.93 | $101 | 6 | 5 |

| biBERK | 3.86 | $103 | 8 | 8 |

| Chubb | 3.73 | $127 | 3 | 4 |

| Progressive Commercial | 3.64 | $112 | 8 | 7 |

How Did We Determine These Rates and Rankings?

These rates are estimates based on MoneyGeek's analysis of small businesses with 1 to 4 employees across 408 major industries. Actual rates vary based on your business location, industry risk factors, claims history, coverage limits and individual insurer underwriting criteria. Contact insurers directly for personalized quotes.

The Hartford

Best Workers' Comp Insurance in Maine

MoneyGeek Rating

4.5/ 5

4.9/5Affordability

4.1/5Customer Experience

4/5Coverage

Average Monthly Rate

$81Claims Processing Score

4.1/5Policy Management Score

4/5Buying Process Score

4/5

Coverdash

Best Maine Workers' Comp Insurance: Runner-Up

MoneyGeek Rating

4.4/ 5

4.7/5Affordability

4/5Customer Experience

4.9/5Coverage

Average Monthly Rate

$89Claims Processing Score

4/5Policy Management Score

4/5Buying Process Score

4/5

LEARN MORE ABOUT MAINE BUSINESS INSURANCE

Learn more about business insurance options in Maine:

Cheapest Workers' Comp Insurance in Maine

The Hartford is Maine's cheapest workers' comp insurance provider at $81/month, but the more useful finding in our data is how tight the top of the field runs. The first five carriers are separated by just $20 per month, a $240 annual difference. For most small businesses in Maine, that spread is narrower than the cost of a single missed workday.

| The Hartford | $81 | $972 |

| ERGO NEXT | $83 | $996 |

| Coverdash | $89 | $1,068 |

| Thimble | $90 | $1,080 |

| Nationwide | $101 | $1,212 |

| Hiscox | $101 | $1,212 |

| biBERK | $103 | $1,236 |

| Simply Business | $107 | $1,284 |

| Progressive Commercial | $112 | $1,344 |

| Chubb | $127 | $1,524 |

Cheapest Workers' Comp Insurance in Maine by Industry

When we pulled rates across 25 industries in Maine, one pattern was impossible to miss: The Hartford is the cheapest option in 19 of them. That kind of consistency across industries as different as financial services and manufacturing is unusual, and it tells you something real about how The Hartford approaches this market.

The Hartford's pricing advantage is widest in low-risk industries. Financial services ($9/month), consulting ($12/month) and marketing ($12/month) are the three cheapest categories in our data. Where ERGO NEXT is cheapest clusters around industries with real physical exposure, like construction ($202/month), recreation and sports ($95/month) and pet care ($54/month). Construction is the priciest category in our entire Maine dataset, which reflects the injury risk profile.

| Agriculture & Natural Resources | The Hartford | $138 | $1,656 |

| Arts, Media & Entertainment | The Hartford | $77 | $924 |

| Beauty, Body & Wellness Services | The Hartford | $11 | $132 |

| Childcare Services | Coverdash | $29 | $348 |

| Cleaning Services | The Hartford | $83 | $996 |

| Construction & Contracting | ERGO NEXT | $202 | $2,424 |

| Consulting Services | The Hartford | $12 | $144 |

| Education | The Hartford | $54 | $648 |

| Financial Services | The Hartford | $9 | $108 |

| Fitness Services | Coverdash | $52 | $624 |

| Food & Beverage | The Hartford | $33 | $396 |

| Healthcare & Medical | The Hartford | $30 | $360 |

| Hospitality, Travel & Tourism | The Hartford | $29 | $348 |

| Manufacturing | The Hartford | $101 | $1,212 |

| Marketing & Communications | The Hartford | $12 | $144 |

| Nonprofit & Associations | The Hartford | $40 | $480 |

| Other Professional Services | The Hartford | $17 | $204 |

| Pet Care Services | ERGO NEXT | $54 | $648 |

| Real Estate & Property Services | The Hartford | $14 | $168 |

| Recreation & Sports | ERGO NEXT | $95 | $1,140 |

| Repair & Maintenance | The Hartford | $60 | $720 |

| Retail & Product Rental | The Hartford | $35 | $420 |

| Tech/IT | The Hartford | $25 | $300 |

| Transportation & Logistics | Coverdash | $250 | $3,000 |

| Wholesale & Distribution | The Hartford | $151 | $1,812 |

How Much Is Workers' Comp Insurance in Maine?

Maine's state average workers' comp cost is $99 per employee per month, well above the $74 national average. Beauty, Body & Wellness Services is the cheapest industry in the state at $15/month, while Transportation & Logistics is the most expensive at approximately $300/month state average. The cheapest provider rate in any given industry will be lower than the state average shown in the table below.

The most counterintuitive finding in this data is where Tech and IT lands. At $42 per month, it matches Hospitality, Travel and Tourism exactly and sits above Financial Services, Marketing and Consulting by $26 per month. That gap reflects how Maine insurers classify hybrid tech roles that include on-site installation, equipment handling or field work alongside desk-based work. If your tech business is fully remote, your actual rate may be lower than this average.

| Beauty, Body & Wellness Services | $15 | $180 |

| Financial Services | $16 | $192 |

| Marketing & Communications | $16 | $192 |

| Consulting Services | $20 | $240 |

| Real Estate & Property Services | $22 | $264 |

| Other Professional Services | $24 | $288 |

| Childcare Services | $36 | $432 |

| Food & Beverage | $40 | $480 |

| Hospitality, Travel & Tourism | $42 | $504 |

| Tech/IT | $42 | $504 |

| Healthcare & Medical | $50 | $600 |

| Retail & Product Rental | $54 | $648 |

| Nonprofit & Associations | $57 | $684 |

| Pet Care Services | $63 | $756 |

| Fitness Services | $64 | $768 |

| Education | $66 | $792 |

| Repair & Maintenance | $73 | $876 |

| Arts, Media & Entertainment | $91 | $1,092 |

| Recreation & Sports | $113 | $1,356 |

| Cleaning Services | $118 | $1,416 |

| Manufacturing | $141 | $1,692 |

| Agriculture & Natural Resources | $162 | $1,944 |

| Wholesale & Distribution | $180 | $2,160 |

| Construction & Contracting | $276 | $3,312 |

| Transportation & Logistics | $300 | $3,600 |

Maine Workers' Comp Insurance Cost Factors

The Maine Workers Compensation Board and the NCCI jointly shape the state's rating environment. NCCI serves as Maine's designated rating bureau, filing loss costs that carriers use as the basis for individual rate multipliers. Maine's competitive state fund structure, anchored by Maine Employers Mutual Insurance Company (MEMIC), adds a layer of market pressure that distinguishes it from states with only private carriers. The state's forestry, fishing and maritime industries drive above-average loss costs in those class codes.

How Much Workers' Comp Insurance Do I Need in Maine?

Maine law requires every private employer to carry workers' compensation coverage starting with your first employee. Coverage amounts scale with total payroll since Maine bases benefits on wages. The maximum weekly benefit is $441 or 125% of the state average weekly wage, whichever is higher. Maine pays two-thirds of lost wages for partial incapacity and 80% of after-tax wages for total incapacity, with medical expenses covered without dollar limits.

Operating without required workers' compensation coverage results in fines up to $10,000 or 108% of unpaid premiums and stop-work orders. Knowing violations constitute criminal charges.

Maine Workers' Comp Insurance Exemptions

Some business categories are exempt from workers' comp requirements:

- Sole proprietors without employees: Automatically excluded from coverage with no waiver form required. Coverage becomes mandatory when hiring employees.

- Self-employed partners: Maine excludes partners from coverage by default. Partners can purchase policies that include partner coverage.

- LLC members: Maine automatically excludes LLC members from workers' comp requirements. Members can add themselves to coverage through their insurance carrier.

- Corporate officers with 20% ownership: Officers owning at least 20% of the corporation's outstanding voting stock can opt out. File a written waiver with the Maine Workers' Compensation Board.

- Family members of business owners: Parents, spouses and children who work for sole proprietors, partners, 20% corporate shareholders or LLC members can waive coverage by submitting a written request to the Board.

- Seasonal or casual farm workers: Exempt when employers maintain at least $25,000 in employer's liability insurance plus $5,000 in medical coverage.

- Small farm operations with six or fewer workers: Exempt when carrying employer's liability insurance of at least $100,000 multiplied by the number of full-time employees, plus $5,000 in medical coverage.

- Small wood harvesting operations: Exempt when harvesting 150 cords of wood or less annually from farm wood lots. Requires $25,000 in liability insurance and $5,000 in medical coverage.

- Domestic service workers: Maine doesn't require coverage for employees performing domestic services in private homes.

- Nonprofit executive officers: Coverage for executive officers of charitable, religious, educational, or other nonprofit corporations depends on the organization's specific policy provisions.

- Nonresident temporary workers: Out-of-state employees working temporarily in Maine don't need coverage if their home state's workers' comp already covers them and the employer has no permanent business location in Maine.

- Independent contractors: Maine law doesn't classify contractors as employees. Workers' comp policies don't cover contractors. Request certificates of insurance from contractors.

FEDERAL WORKERS' COMP PROGRAMS OVERRIDE STATE REQUIREMENTS

Three federal programs supersede Maine's state workers' comp requirements for specific worker categories. The Federal Employees' Compensation Act (FECA) covers civilian federal employees, including those at Maine's federal facilities and military installations. The Federal Employers' Liability Act (FELA) covers railroad workers engaged in interstate commerce. The Longshore and Harbor Workers' Compensation Act covers maritime and port workers, which is particularly relevant given Maine's active commercial fishing ports and harbor facilities in Portland, Rockland and other coastal communities. Employers with workers in any of these categories should confirm federal program applicability before relying on a state policy.

How to Get the Best Workers' Comp Insurance in Maine

Follow these seven steps to secure the right workers' comp coverage for your Maine business.

- 1

Confirm Your Coverage Obligation

Verify whether your Maine business meets the coverage threshold. Maine requires workers' comp for employers with one or more employees. The Maine Workers Compensation Board administers the requirement and can confirm whether your business structure triggers the obligation.

- 2

Identify Your Industry Class Codes

Maine uses NCCI class codes to classify employees by occupation and risk level. Verify your payroll classification before requesting quotes, as an incorrect class code assignment can result in a large premium adjustment at your annual audit.

- 3

Compile Payroll and Loss History

Gather three years of loss runs and payroll records organized by class code. Clean loss history improves your rate position in the voluntary market. Carriers including The Hartford and Coverdash will use this data to generate accurate quotes for your Maine business.

- 4

Request Quotes from Multiple Carriers

Include The Hartford (Maine's lowest-rate provider at $81/month), Coverdash ($89/month) and Thimble ($90/month) in your comparison. Also request a quote from Maine Employers Mutual Insurance Company (MEMIC), the competitive state fund that holds a primary position in the Maine market. Comparing at least three carriers gives you a reliable rate range.

- 5

Evaluate Coverage Breadth Alongside Rate

Coverdash earns strong marks for coverage breadth in Maine and is worth prioritizing when your industry requires broader endorsements or specialty coverage. Rate alone should not drive the decision, particularly for employers in higher-hazard industries where claims frequency is greater.

- 6

Bind Coverage and File with Maine Workers Compensation Board

Coverage must be in place before employees begin work. Maintain your certificate of insurance and provide proof of coverage to any general contractors or clients who require it. File all required documentation with the Maine Workers Compensation Board before your employees' first day.

- 7

Prepare for the Annual Payroll Audit

Maine workers' comp policies are audited annually. Employers in seasonal industries, including fishing, agriculture and ski resort operations, should maintain detailed payroll records by class code throughout the year. Accurate records reduce the risk of a large premium adjustment at audit.

Bottom Line and Next Steps

The Hartford and Coverdash are Maine's top workers' comp providers, but the right choice depends on your business profile. The Hartford is the strongest option for most Maine small businesses, combining the lowest rate with the highest MoneyGeek score. Coverdash is a better fit when coverage breadth matters more than rate, earning the runner-up position through strong coverage scores and digital accessibility.

Next Steps

Maine workers' comp rates vary more than in many states because of the state's wide industry mix, from low-hazard professional services to high-hazard maritime and forestry work. Getting multiple quotes is the most reliable way to find your actual rate.

Maine Workers' Compensation Insurance FAQs

What are the penalties for not having workers' comp insurance in Maine?

Maine employers without required workers' comp coverage may face civil fines, stop-work orders and personal liability for all injury costs sustained by uninsured workers. The Maine Workers Compensation Board enforces compliance and can issue stop-work orders that halt business operations until coverage is obtained.

Does Maine workers' comp cover remote or work-from-home employees?

Yes. Maine workers' comp covers employees who work from home if the injury occurs in the course of employment. The injury must arise out of and in the course of the employee's work duties. Employers should confirm that their policy reflects the actual work locations of all covered employees.

How does an experience modification rate affect Maine workers' comp premiums?

Maine uses the NCCI experience modification rating (EMR) system. An EMR above 1.0 increases your premium; an EMR below 1.0 reduces it. Employers with three or more years of loss history receive an EMR that reflects their claims record relative to their industry. A single large claim can raise your EMR and increase premiums for up to three subsequent policy years.

Can owners and officers opt out of workers' comp coverage in Maine?

Officers of closely held corporations may elect to exclude themselves from workers' comp coverage in Maine, subject to the Maine Workers Compensation Board's statutory requirements for the election. Sole proprietors without employees are generally not required to carry coverage for themselves but may elect to do so voluntarily.

What is the difference between workers' comp and employer's liability in a Maine policy?

Workers' comp covers your statutory obligation to pay medical and wage benefits to injured employees. Employer's liability, which is Part Two of a standard workers' comp policy, covers lawsuits brought by employees who claim their injury resulted from employer negligence and falls outside the exclusive remedy of workers' comp. Both coverages are typically included in a single Maine workers' comp policy.

How long does a workers' comp claim stay on a Maine employer's experience record?

Under NCCI rules, which apply in Maine, a workers' comp claim affects an employer's experience modification rating for three policy years after the year in which the claim occurred. Claims are removed from the EMR calculation after that period, though large losses may have a longer practical effect on carrier underwriting decisions.

MoneyGeek analyzed workers' comp insurance rates and provider performance across Maine using small business profiles with 1 to 4 employees spanning 408 major industries. Companies earn up to five points in each category in our scoring system. We then use a weighted average of these category scores to calculate a MoneyGeek score out of five.

- Affordability (55%): Based on average payroll for the most common employee code per industry and state classification, priced per employee for a 1 to 4 employee business.

- Customer Experience (35%): Evaluates buying (20%), which covers quote access, pricing accuracy and sales support; policy management (30%), which covers payroll reporting, audits, billing and loss control; and claims (50%), which covers FNOL speed, adjuster support, medical access, wage replacement and dispute handling.

- Coverage Options (10%): Assesses coverage completeness (35%), including employers' liability and wage and medical reimbursement; policy flexibility and endorsements (25%); eligibility, state and industry breadth (20%); and policy terms, limits and exclusions (20%).

About Connor Bolton

Connor Bolton is Senior SEO and Content Manager at MoneyGeek, where he leads the business and pet insurance editorial teams. He sets the research framework, data standards and content structure for his team. All content goes through his accuracy review before publication. Connor also writes in-depth guides and has spent more than four years covering insurance products across personal, commercial and specialty lines.

The research infrastructure Connor built covers auto, home, renters, life, health, business and pet insurance across pricing analysis, carrier research, customer experience and coverage evaluation. It includes over 6 million data points for business insurance across 408 industry areas, all 50 states and 16 vehicle types. The pet insurance side covers over 5 million profiles across 18 major providers, 100+ breeds and ages up to 20 years. Connor’s insurance research and his team's work has been cited by the U.S. Chamber of Commerce, Allstate, Liberty Mutual, CBS News, Forbes and LegalZoom.

Connor also talks with underwriters and carrier liaisons at Ethos, The Hartford, ERGO NEXT, Nationwide and State Farm, and monitors business and pet owner communities on Reddit. Those sources shape how his team evaluates carriers, structures rate analysis and writes for human buyers rather than search engines.

For questions about MoneyGeek's business and pet insurance content, contact him at connor@moneygeek.com or on LinkedIn.

Sources

- Insurance Journal. "Maine Approves 9.6% Decrease in Workers' Compensation Costs." Accessed June 21, 2026.

- Maine Bureau of Insurance. "Maine Bureau of Insurance Approves 9.6% Average Decrease in Workers' Compensation Loss Costs." Accessed June 21, 2026.

- Maine Bureau of Insurance. "Maine's Bureau of Insurance Approves 19% Average Decrease in Workers' Compensation Loss Costs." Accessed June 21, 2026.

- Maine Legislature. "Title 39-A, §211: Maximum Benefit Levels." Accessed June 21, 2026.

- Maine Legislature. "Title 39-A, §212: Compensation for Total Incapacity." Accessed June 21, 2026.

- Maine Legislature. "Title 39-A, §213: Compensation for Partial Incapacity." Accessed June 21, 2026.

- Maine Legislature. "Title 39-A, §324: Compensation Payments; Penalty." Accessed June 21, 2026.

- Maine Legislature. "Title 39-A, §401: Liability of Employer." Accessed June 21, 2026.