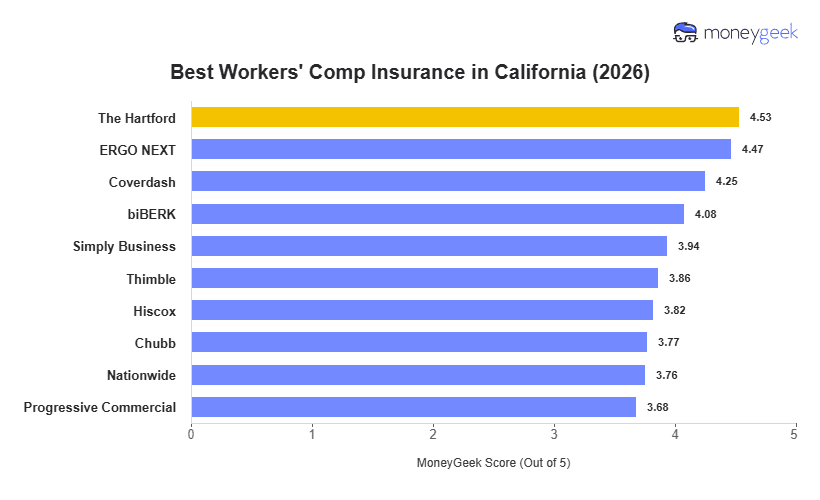

The Hartford leads California workers' comp rankings with the top MoneyGeek score, combining the second-highest affordability score in the state with a strong claims performance ranking. ERGO NEXT ranks second with the lowest overall monthly rate among all California providers at $188 per employee.

The rate spread between ERGO NEXT ($188 a month) and the most expensive provider, Progressive Commercial ($286 a month), is $98. California's rate range is compressed relative to the dollar spread because all carriers face the same elevated California loss costs. For professional-sector employers, the rate advantage at the low end is most pronounced in financial services and consulting categories.