Painting ranks 17th in affordability within its general industry category, and 339th compared to all other areas of work, in MoneyGeek's analysis of contractor insurance costs. $183 a month is the average monthly rate that comes out to, slightly below the $190 a month national average for its work category, but well above the $111 a month national average overall.

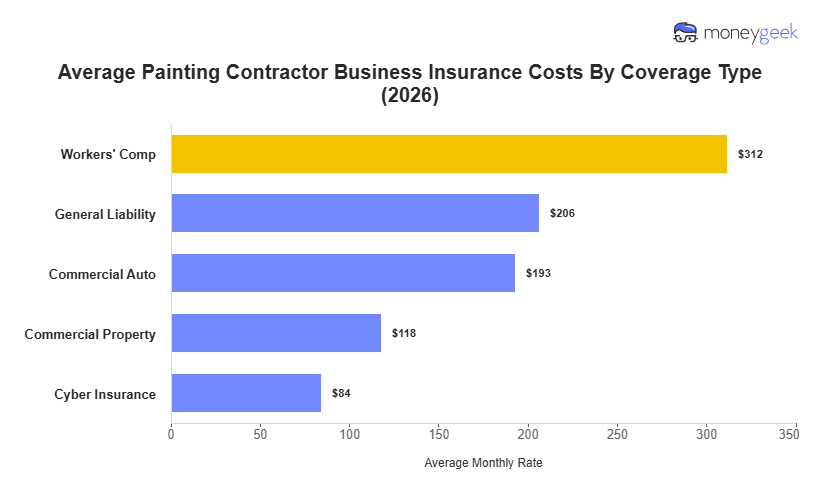

Workers' comp ($312 a month per employee) and general liability ($206 a month) cost the most among contracting coverage types, like any other contracting work, because of high public exposure, the risks that come with frequently changing clients, especially in residential work, and the chance of fall injuries while painting home exteriors or high-rise interior walls.

Commercial property, cyber and commercial auto policies land more toward the middle of the spectrum, but each can rise past benchmarks on its own trigger: specialized equipment for commercial property, extensive stored customer data for cyber, and more frequent or longer-distance driving for commercial auto.