HVAC contractors average $197 per month or $2,361 annually, across six common coverage types, based on MoneyGeek's analysis of quotes for businesses with one to four employees, across 50 states plus DC, with $1 million per occurrence limits. Among contractor business insurance costs, HVAC contractors rank 23 out of 45, toward the middle of the category, not at the high end.

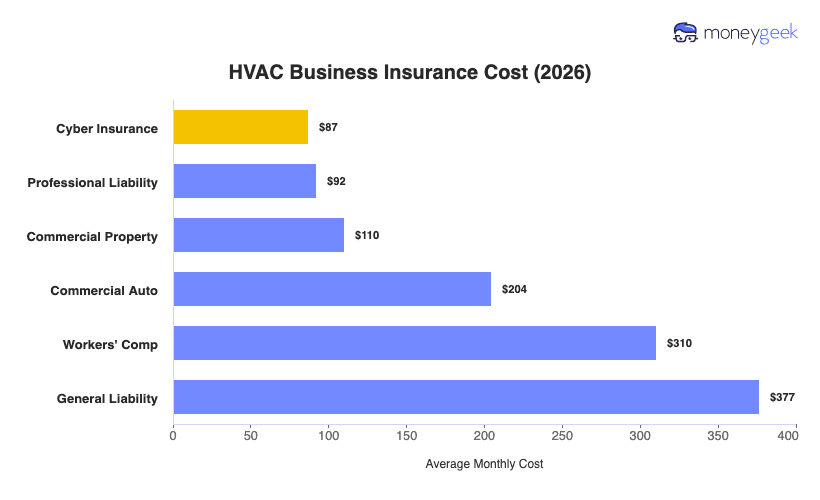

Per-coverage costs run $87 to $377 per month. Cyber anchors the low end, since most HVAC operations carry limited digital exposure relative to other industries. General liability sits highest because your crews work inside occupied buildings on mechanical systems where installation errors and on-site injuries generate third-party claims quickly.

The table below shows the full breakdown, but treat these figures as benchmarks, since your premium varies with your specific profile.