Cleaning business insurance cost for pressure washers averages $92 per month, or $1,107 per year, based on MoneyGeek's analysis. Pressure washing ranks 11th in affordable among cleaning sub-industries, which reflects its chemical exposure, mobile operations and heavier equipment.

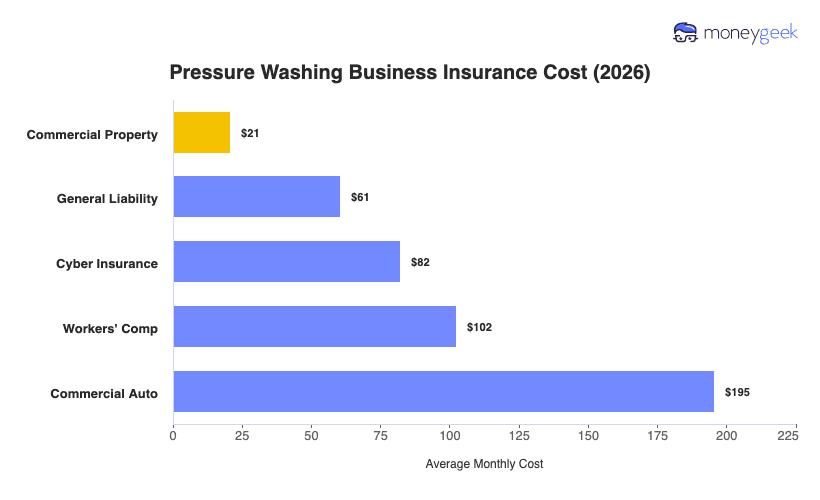

Per-policy costs range from $21 per month for commercial property to $195 for commercial auto. Commercial property is the least expensive, averaging $21 per month, because your pressure washer, surface cleaner and trailer carry known replacement costs with no payroll exposure or third-party injury risk factored in. Commercial auto sits highest because your truck and trailer are on the road for every job, and insurers build that constant movement into the rate.

The figures in the table below are benchmarks, not quotes as your actual premium shifts with crew size, location and the services you offer.