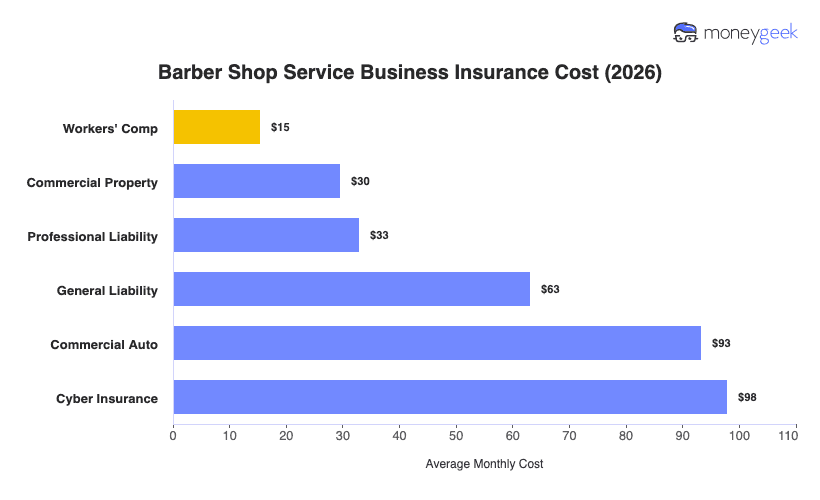

If you run a brick-and-mortar dog grooming shop, you're looking at an average of $59 per month ($709 per year) across the six most common coverage types. Based on MoneyGeek's analysis of small business insurance cost, that's on the lower end for pet care businesses, largely because your fixed location carries a more predictable risk footprint than mobile operations or facilities that board animals overnight.

Individual policy costs range from $30 to $102 per month. Professional liability is the least expensive, because grooming advice and service-error claims rarely reach litigation at a fixed shop. Commercial auto costs the most, though that only applies if your shop operates a vehicle for pickups or deliveries. Use these figures as benchmarks, not quotes, since your actual premium depends on your payroll, shop location, claims history and the limits you select.

The table below breaks down all six coverage types: