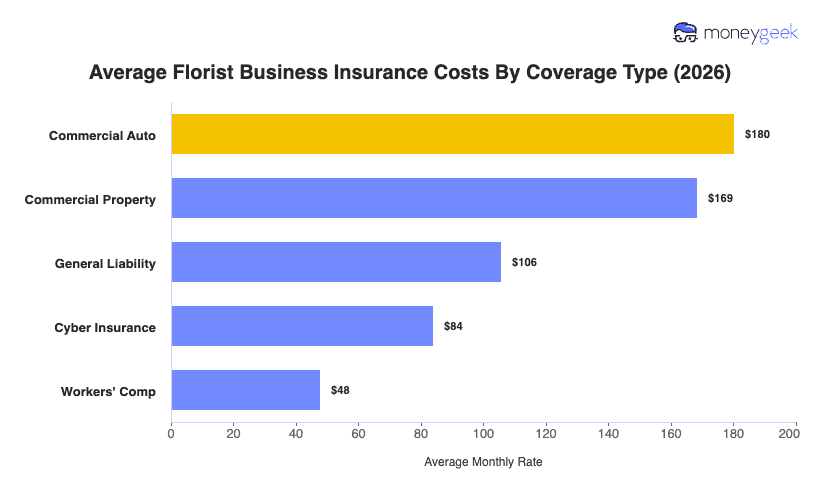

Retail business insurance costs for florists sits in the lower end of pricing at $117 per month, or $1,408 per year within its work sector at 15th in terms of affordability. Compared to the national average of $113/mo it is only slightly higher on average across the five coverage types most small flower shops will need. At the coverage level, the story gets clearer, and it clearly aligns with the industry's risk.

Commercial property and auto policies lead as the most expensive due to risks involved with frequent delivery of floral arrangements, the cost of equipment that keep flowers alive and thriving, and the inherent risks of someone stealing goods or damaging property in any store environment (from delivery people or customers). While general liability is below the national average at $106/mo (versus $123/mo nationally), there are still common claims associated with someone slipping on water and getting injured due to your need to watering plants throughout the day. Workers' comp is not expensive at all since the work is not physically demanding and cyber is only modestly priced.