Business insurance costs for moving companies average $338 per month, or about $4,060 per year, based on our team's analysis of quotes for movers with less than five employees across five coverage types, 16 commercial vehicle types and all 50 states plus DC carrying limits of $1 million per occurrence and $2 million aggregate. I found that moving companies cost more 71% of business types within the transportation and logistics cluster.

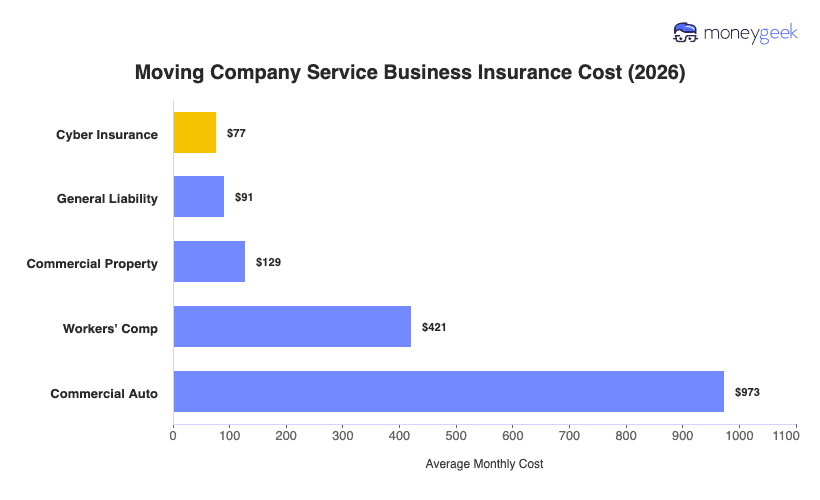

Individual coverage types range from $77 to $973 per month, a difference that reflects how differently insurers price your risks. Cyber insurance is the most affordable because your customer data exposure, while real, isn't something you encounter on daily basis. You'll pay the most for commercial auto insurance because your trucks are on the road every day with cargo carries third-party liability on each job.

The breakdowns in the table below are benchmarks, not quotes, as your actual premiums vary by fleet size, payroll, driving history and state: