The cost of business insurance for candle makers averages $116 per month, or $1,397 per year, across the five most common coverage types for businesses with one to four employees across 50 states and Washington, D.C.

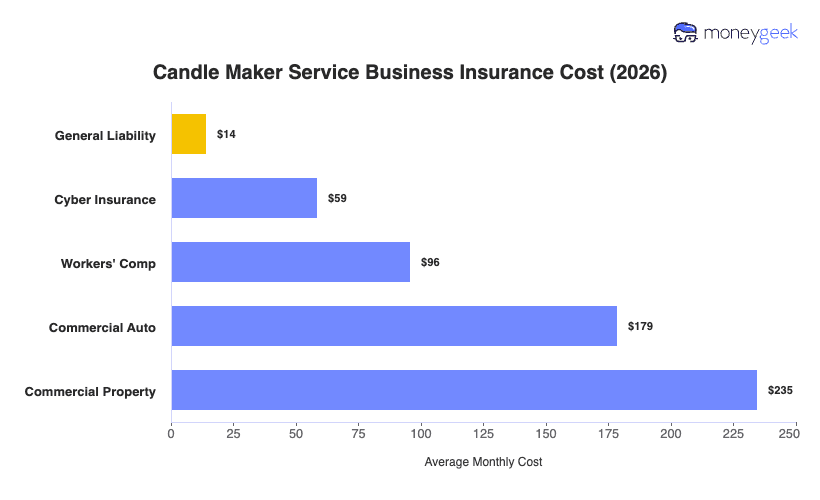

Your actual cost per policy depends the coverage type you're looking at. General liability runs around $14 per month for candle makers, affordable partly because most operations are small-scale and partly because product liability risk is priced into the policy rather than purchased separately. Commercial property sits at the other end at around $235 per month, driven by the value of flammable inventory, fragrance stock and glass container goods concentrated in your production space.

The table below breaks down per-coverage estimates, but treat these figures as reference points, not quotes, since your actual premium depends on your production setup, sales volume and claims history.