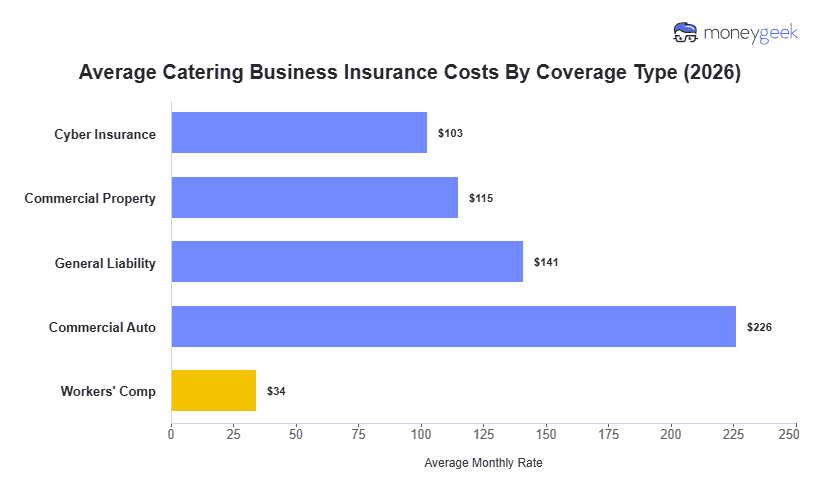

The average cost of food business insurance varies across business types. For catering businesses, estimates average $124 per month, or $1,485 per year, based on five common coverage types for catering businesses with one to four employees across 50 states and Washington, D.C., at $1 million per occurrence and $2 million aggregate limits.

Individual policies range from $34 to $226 per month. Workers' comp prices low because catering operations run on part-time event staff hired per booking, keeping payroll exposure modest. Commercial auto runs highest as caterers load vans and box trucks with food, equipment and staff for off-site events, and insurers price that exposure on vehicle type and use frequency. Monthly costs by coverage type appear in the table below.