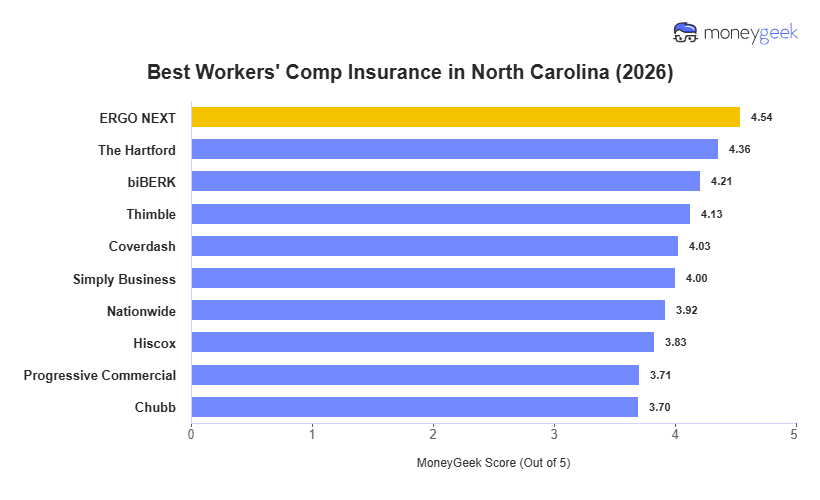

ERGO NEXT is the top workers' comp insurer in North Carolina, combining the lowest available rate with strong customer experience scores. The Hartford and biBerk follow as reliable runner-up options for North Carolina small businesses.

The $54 a month spread between cheapest provider, ERGO NEXT ($62), and the most expensive provider, Chubb ($116), represents $648 in potential annual per-employee savings. That gap is most actionable for businesses in lower-risk industries with clean claims histories.