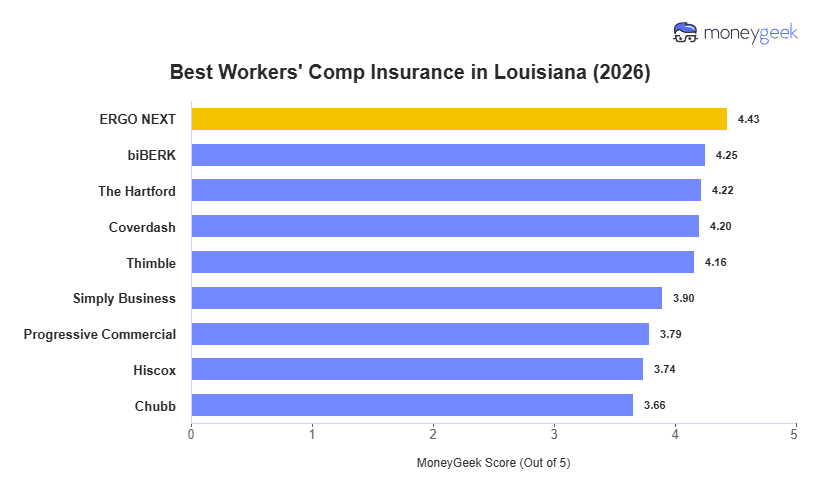

ERGO NEXT has the best workers' compensation insurance in Lousisiana with the top MoneyGeek score and lowest monthly rates among providers we reviewed. biBERK, The Hartford and Coverdash offer strong alternatives in the state.

ERGO NEXT is Louisiana's cheapest provider at $85/month. Chubb is the most expensive at $143/month, creating a $58 spread between the lowest and highest provider averages. Low-hazard professional employers benefit most from ERGO NEXT's rate advantage, but the gap between provider rates narrows for high-hazard class codes where Chubb's coverage depth may justify the higher premium.