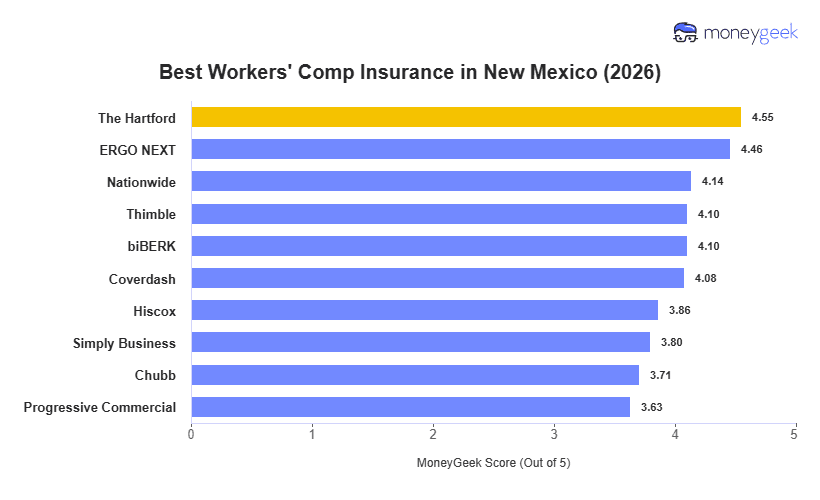

The Hartford is the top workers' comp provider in New Mexico, combining a low $64/month rate with strong customer experience and competitive coverage options. ERGO NEXT matches that rate and stands out as a strong runner-up, while Nationwide offers a reliable alternative for employers seeking a more widely recognized carrier.

The $46 monthly gap between the cheapest and most expensive providers in our analysis amounts to as much as $552 per employee annually. For a business with four employees, that difference adds up to $2,208 per year, highlighting the importance of comparing quotes across providers.