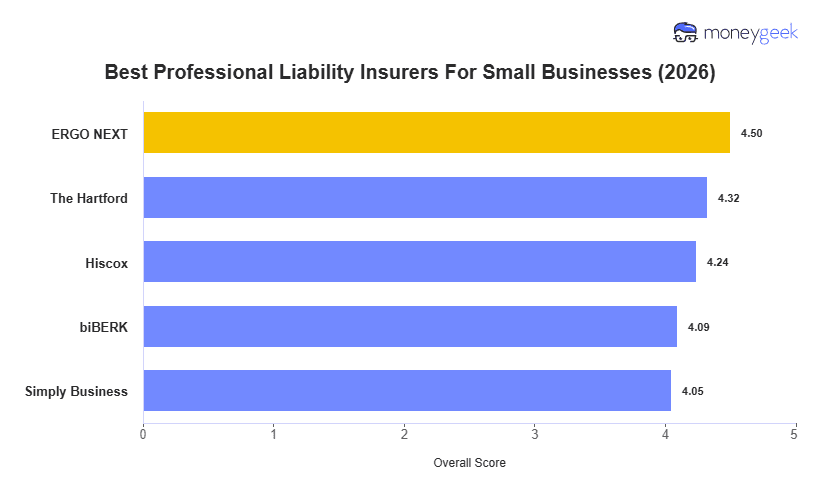

MoneyGeek analyzed major commercial insurers across the United States and identified these providers as the strongest professional liability offerings:

- ERGO NEXT: Places first overall and leads among B2C industries, with competitive pricing across most business profiles, strong service from purchase through claims and adaptable coverage options.

- The Hartford: Offers the lowest rates among established insurers and carries the top-rated claims experience in MoneyGeek's analysis, performing particularly well for consultants and financial professionals.

- Hiscox: Delivers strong value for beauty services and nonprofits through specialized coverage packages tailored to select industries.

- biBerk: Places second overall for the online buying experience and holds top ratings for underwriting transparency and sales support quality.

- Simply Business: The aggregator model works well for businesses comparing multiple providers simultaneously. Simply Business carries the broadest coverage selection and most flexible professional liability options, with rates that particularly favor cleaning companies.

The five-insurer comparison is detailed in the table below.