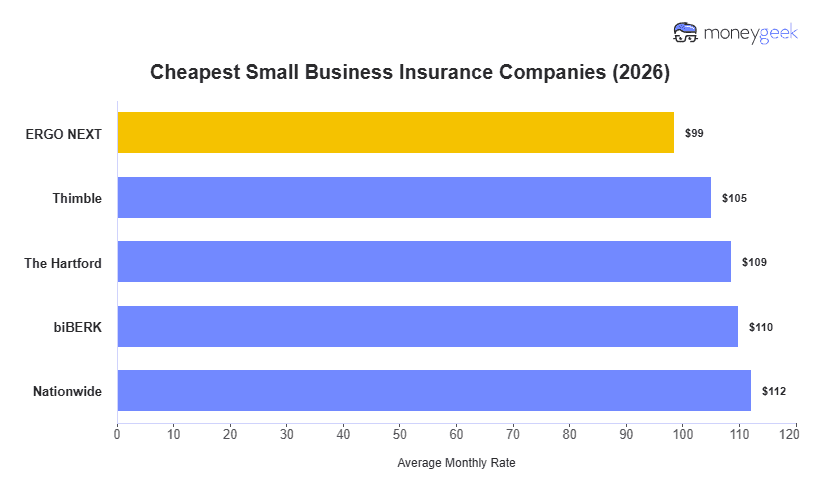

I found ERGO NEXT offers the lowest small business insurance rate nationwide at $99/mo, saving you 11% compared to the national composite average of $111/mo. Thimble, The Hartford, biBerk and Nationwide follow behind to round out my cheapest providers list. If you're looking for event and job-level coverage, Thimble will likely edge out the competition since they offer coverage by the hour, making it much easier to save.

My picks are based on aggregated rates from the six most common types of small business insurance across 400+ industries, all states (including D.C.), employee counts from 0 to 49 and 16 vehicle types (for commercial auto pricing). So, in other words, it is a high-level representation of who has the lowest rates nationally and may not be affordable for your business's profile or specific coverage needs. For example, while ERGO NEXT is the national winner, at the coverage type level, they only rank first in affordability for workers' comp.