ERGO NEXT ranks first for professional liability insurance in Nebraska with competitive rates, top-rated customer service and a streamlined digital platform that gets you covered in minutes. As the cheapest professional indemnity insurer in Nebraska, The Hartford offers policies averaging $68 monthly, $5 below the state average. Simply Business, Coverdash and Nationwide also earn high marks for Nebraska businesses seeking quality errors and omissions coverage.

Best Professional Liability Insurance in Nebraska

Get NE professional liability insurance quotes starting at $26 monthly from MoneyGeek's top companies like ERGO NEXT, The Hartford and Simply Business.

Get matched to the best professional liability insurance in NE for you below.

Select your industry

Select state

Updated: March 16, 2026

Advertising & Editorial Disclosure

Professional Liability Insurance in Nebraska: Key Takeaways

ERGO NEXT provides the best professional liability insurance in Nebraska, while The Hartford delivers the most affordable coverage starting at $68 monthly (Read More).

Professional liability insurance costs in Nebraska average $73 monthly ($881 annually), placing the state among the more affordable options nationwide (Read More).

Professional liability insurance protects Nebraska businesses from financial losses due to professional mistakes, missed deadlines and claims of inadequate work performance (Read More).

Nebraska doesn't mandate professional liability insurance for most businesses, though health care providers and certain licensed professionals must maintain coverage (Read More).

Nebraska business owners should request small business insurance quotes from multiple providers to secure optimal professional liability coverage at competitive rates (Read More).

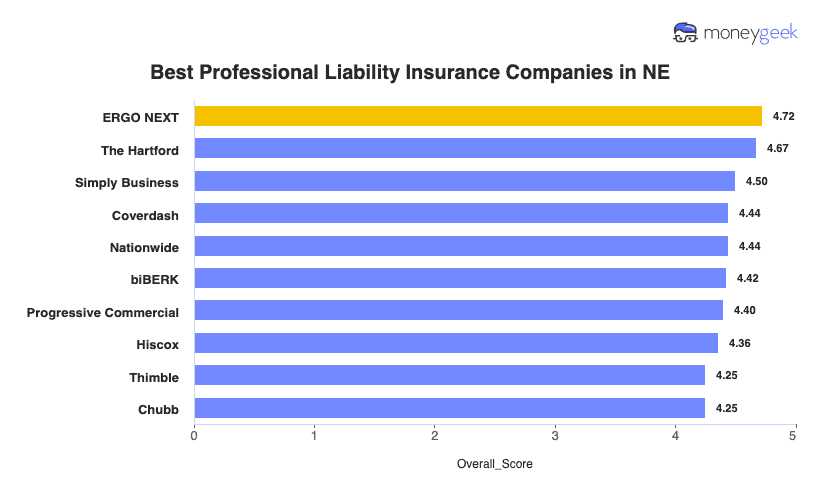

Best Professional Liability Insurance Companies in Nebraska

| ERGO NEXT | 4.72 | $69 |

| The Hartford | 4.67 | $68 |

| Simply Business | 4.50 | $72 |

| Coverdash | 4.44 | $73 |

| Nationwide | 4.44 | $78 |

| biBERK | 4.42 | $75 |

| Progressive Commercial | 4.40 | $71 |

| Hiscox | 4.36 | $73 |

| Thimble | 4.25 | $72 |

| Chubb | 4.25 | $84 |

How Did We Determine the Best Professional Liability Insurance in Nebraska?

These rates are estimates based on MoneyGeek's proprietary analysis of small businesses with two employees across 79 major industries and should not be considered quotes. Your actual rate will differ based on business-specific factors. Contact insurers directly for accurate pricing tailored to your business needs.

LEARN MORE ABOUT BUSINESS INSURANCE IN NEBRASKA

Beyond professional liability insurance in Nebraska, we've provided the following state-specific resources to get the best coverage for your business:

1. ERGO NEXT: Best Professional Liability Insurance in NE

pros

Ranks first for customer service in Nebraska

Get coverage and instant certificates in 10 minutes

Coverage tailored to your specific professional risks

Second-lowest rates for professional liability in Nebraska

Personalized coverage matching for both types and limit amounts

cons

Less than 10 years in business

Claims process ranks lower than other providers

COMPANY HIGHLIGHTS

Small business owners in Nebraska save $4 monthly with ERGO NEXT while avoiding the hassles traditional insurers create. An Omaha consultant can secure client contract approval overnight instead of waiting three days for agent callbacks, while a Lincoln architect meets licensure deadlines without paperwork delays. You'll customize your coverage and download certificates at 2 a.m. before tomorrow's client meeting.

2. The Hartford: Cheapest Professional Liability Insurance in NE

pros

Lowest rates for professional liability insurance in NE

Best claims handling and agent service ratings from customers

Great personalized E&O coverage options for tech, law and medical professionals

A+ Superior financial strength rating from AM Best

cons

Digital experience ranks 10th nationally

Requires agent contact for some policy changes

COMPANY HIGHLIGHTS

Nebraska business owners pocket $65 annually with The Hartford's $68 monthly rates, the lowest in the state. An Omaha accountant saves that $65 instead of paying the state average, while a Lincoln consultant gets claim checks faster when mistakes happen. The Hartford ranks first nationally for claims handling and customer satisfaction, meaning you'll spend less time fighting for reimbursement and more time running your business.

3. Simply Business: Best Professional Liability Insurance Coverage Options in NE

pros

Ranks first for coverage options, with 16+ carrier partners

Ranks third for digital experience, with 24/7 certificate access

Reliable claim payments backed by Travelers' A++ Superior rating

Broker model finds coverage when direct insurers reject you

cons

Ranks eighth for claims processing

Ranks seventh for customer satisfaction

Professional liability coverage costs more than other providers

COMPANY HIGHLIGHTS

Simply Business's 16-carrier broker network gives Nebraska business owners coverage options direct insurers can't match. An Omaha consultant rejected for high-risk tech work gets approved through specialized carriers, while a Lincoln contractor bundles professional liability with cyber coverage and tools insurance in one quote. You'll compare policies from 16+ insurers in 10 minutes instead of calling each one separately. If standard policies don't fit, Simply Business finds specialized coverage that does.

Average Cost of Professional Liability Insurance in Nebraska

Professional liability insurance costs in Nebraska vary by industry. Home-based businesses pay the lowest rates at around $35 per month, while mortgage brokers face the highest average costs at approximately $156 per month. Use the filtering tool below to find specific pricing for your industry and get accurate rates for your business type.

Data filtered by:

Select

| Accountants | $141 | $1,692 |

| Ad Agency | $94 | $1,131 |

| Auto Repair | $77 | $920 |

| Automotive | $71 | $857 |

| Bakery | $50 | $599 |

| Barber | $40 | $483 |

| Beauty Salon | $46 | $549 |

| Bounce House | $55 | $660 |

| Candle | $40 | $475 |

| Cannabis | $118 | $1,411 |

| Catering | $74 | $887 |

| Cleaning | $52 | $623 |

| Coffee Shop | $57 | $683 |

| Computer Programming | $99 | $1,187 |

| Computer Repair | $60 | $718 |

| Construction | $73 | $879 |

| Consulting | $101 | $1,218 |

| Contractor | $60 | $726 |

| Courier | $48 | $575 |

| DJ | $43 | $514 |

| Daycare | $103 | $1,233 |

| Dental | $80 | $959 |

| Dog Grooming | $53 | $633 |

| Drone | $100 | $1,200 |

| Ecommerce | $60 | $717 |

| Electrical | $61 | $727 |

| Engineering | $99 | $1,190 |

| Excavation | $64 | $769 |

| Florist | $35 | $424 |

| Food | $104 | $1,248 |

| Food Truck | $55 | $661 |

| Funeral Home | $75 | $900 |

| Gardening | $38 | $454 |

| HVAC | $78 | $938 |

| Handyman | $50 | $604 |

| Home-based business | $35 | $418 |

| Hospitality | $69 | $824 |

| Janitorial | $47 | $566 |

| Jewelry | $59 | $706 |

| Junk Removal | $64 | $764 |

| Lawn/Landscaping | $48 | $577 |

| Lawyers | $138 | $1,654 |

| Manufacturing | $57 | $682 |

| Marine | $84 | $1,007 |

| Massage | $99 | $1,193 |

| Mortgage Broker | $156 | $1,876 |

| Moving | $78 | $940 |

| Nonprofit | $48 | $579 |

| Painting | $60 | $716 |

| Party Rental | $53 | $631 |

| Personal Training | $67 | $808 |

| Pest Control | $89 | $1,067 |

| Pet | $42 | $510 |

| Pharmacy | $53 | $641 |

| Photography | $61 | $726 |

| Physical Therapy | $87 | $1,048 |

| Plumbing | $86 | $1,035 |

| Pressure Washing | $53 | $638 |

| Real Estate | $119 | $1,428 |

| Restaurant | $78 | $932 |

| Retail | $52 | $618 |

| Roofing | $92 | $1,099 |

| Security | $96 | $1,155 |

| Snack Bars | $46 | $554 |

| Software | $89 | $1,070 |

| Spa/Wellness | $104 | $1,252 |

| Speech Therapist | $93 | $1,112 |

| Startup | $68 | $819 |

| Tech/IT | $93 | $1,112 |

| Transportation | $88 | $1,060 |

| Travel | $91 | $1,090 |

| Tree Service | $71 | $855 |

| Trucking | $104 | $1,253 |

| Tutoring | $58 | $694 |

| Veterinary | $112 | $1,348 |

| Wedding Planning | $71 | $855 |

| Welding | $73 | $872 |

| Wholesale | $58 | $700 |

| Window Cleaning | $59 | $709 |

How Did We Determine These Nebraska Professional Liability Insurance Rates?

These rates are estimates based on MoneyGeek's proprietary analysis of small businesses with two employees across 79 major industries and should not be considered quotes. Your actual rate will differ based on business-specific factors. Contact insurers directly for accurate pricing tailored to your business needs.

What Does Nebraska Professional Liability Insurance Cover?

Professional liability insurance in Nebraska protects your business when clients claim you made mistakes or failed to deliver promised services. This coverage covers both the costs of liability damages and the legal fees associated with defending these claims.

You might see this same type of insurance called by different names:

- Errors and omissions insurance (E&O)

- Malpractice insurance (used mainly in health care and law)

- Professional indemnity insurance

How Much Professional Liability Insurance Do I Need in Nebraska?

Nebraska doesn't require professional liability insurance for most businesses. Health care providers must carry $800,000 per occurrence and $3 million aggregate to qualify for Nebraska's Excess Liability Fund coverage. Law firms organized as professional entities need $250,000 per claim multiplied by the number of attorneys. Most client contracts require $1 million per occurrence and $2 million aggregate coverage.

Who Needs Professional Liability Insurance in Nebraska?

Professionals handling client contracts or facing professional negligence claims should consider professional liability insurance in Nebraska. Client agreements often require proof of coverage before work begins, particularly in health care, consulting and licensed professions.

Agricultural consultants

Nebraska ranks second nationally in cattle production and generates $31.6 billion in agricultural cash receipts, creating liability exposure for crop advisors, agriculture consultants and precision farming specialists. When drought predictions prove wrong or pesticide recommendations damage yields, financial losses can trigger costly lawsuits against the professionals who provided guidance.

Health care professionals

Nebraska requires health care providers to carry $800,000 per occurrence and $3 million aggregate coverage to qualify for the state's Excess Liability Fund. Physicians, nurses and other medical professionals practicing without this coverage risk license suspension and unlimited personal liability for malpractice claims.

Tech Professionals

Omaha's status as the telecommunications capital of the United States, identified by the Federal Reserve Bank of Kansas City, has created a thriving IT sector where data breaches and system failures carry massive financial consequences. Tech E&O insurance protects software developers, IT consultants and cybersecurity specialists when clients claim your work caused their network outage or data loss.

Accountants

Nebraska's Board of Public Accountancy licenses CPAs who serve the state's finance and insurance sector, the state's largest GDP contributor at $31.83 billion, plus diverse manufacturing and agriculture clients. Accountants' professional liability insurance covers claims arising from tax errors, audit mistakes or missed filing deadlines that cost clients money or trigger IRS penalties.

Real estate professionals

The Nebraska Real Estate Commission mandates errors and omissions insurance for real estate as a licensing condition for all brokers and salespersons. Coverage protects against claims stemming from disclosure failures, contract mistakes or property valuation errors during transactions.

Construction contractors

Nebraska's expanding food processing industry and manufacturing growth drive construction demand, particularly in Lincoln and rural areas. General contractors, electricians and HVAC specialists need professional liability coverage when design recommendations, building code interpretations or project management decisions lead to structural failures or costly rework.

How to Get the Best Professional Liability Insurance in Nebraska

Our step-by-step guide walks you through how to get business insurance in Nebraska that matches your professional liability coverage needs and budget. Follow these six steps to secure the right protection for your business.

- 1

Assess your professional liability insurance coverage needs

Understand your business risks and client requirements. A Lincoln CPA serving Nebraska's $31.6 billion agriculture sector has a different liability exposure than an Omaha software developer building systems for the state's telecommunications hub.

- 2

Work with a local agent

Look for an agent who understands Nebraska's goods-producing economy and how business insurance costs differ between urban and rural areas. Agents familiar with Omaha's call center industry can explain coverage needs that don't apply to Grand Island food processing consultants.

- 3

Get quotes and compare coverage details

Request quotes from at least three insurers, comparing both affordable business insurance rates and policy terms like exclusions and deductibles. A Kearney engineer working on meat processing facility designs should examine whether policies cover agricultural industry risks, not just compare premium costs.

- 4

Research the best providers

Beyond price, find insurers experienced with Nebraska's mix of agriculture, manufacturing and financial services. Check AM Best ratings and prioritize carriers with proven claims handling in your specific industry since food processing liability differs from tech consulting.

- 5

Consider bundling discounts

Nebraska's concentration of small agricultural and manufacturing businesses makes bundling valuable, as many operations need both professional liability and equipment coverage. A North Platte precision agriculture consultant saves 20% annually by bundling types of business insurance, including professional liability, general liability and inland marine coverage for farm equipment.

- 6

Don't let your coverage lapse

Claims-made policies dominate Nebraska's professional liability market, meaning you're only covered for claims filed during active policy periods regardless of when the work occurred. A Fremont engineering consultant switching from one carrier to another should purchase tail coverage (extended reporting coverage) to protect against claims from past agricultural facility projects.

Get Nebraska Professional Liability Insurance Quotes

MoneyGeek matches you to top professional liability insurers who understand Nebraska's unique business landscape. Use our tool below to find the right provider for your industry and get personalized quotes tailored to your coverage needs.

Get Matched to the Best NE Professional Liability Insurer for You

Select your industry and state to get a customized NE professional liability insurer match and get tailored quotes.

Industry

State

Nebraska Professional Liability: Bottom Line

Finding the right professional liability insurance in Nebraska starts with understanding your business risks and client contract requirements. ERGO NEXT earns our top rating, but your industry, coverage needs and budget determine the best choice for your situation. Compare quotes from multiple insurers, then work with an agent who understands Nebraska's agriculture, manufacturing, and service sectors to secure coverage that financially protects your business.

About Mark Fitzpatrick

Mark Fitzpatrick, a Licensed Property and Casualty Insurance Producer, is MoneyGeek's resident Personal Finance Expert. He has analyzed the insurance market for over five years, conducting original research for insurance shoppers. His insights have been featured in CNBC, NBC News and Mashable.

Fitzpatrick holds a master’s degree in economics and international relations from Johns Hopkins University and a bachelor’s degree from Boston College. He's also a five-time Jeopardy champion!

He writes about economics and insurance, breaking down complex topics so people know what they're buying.