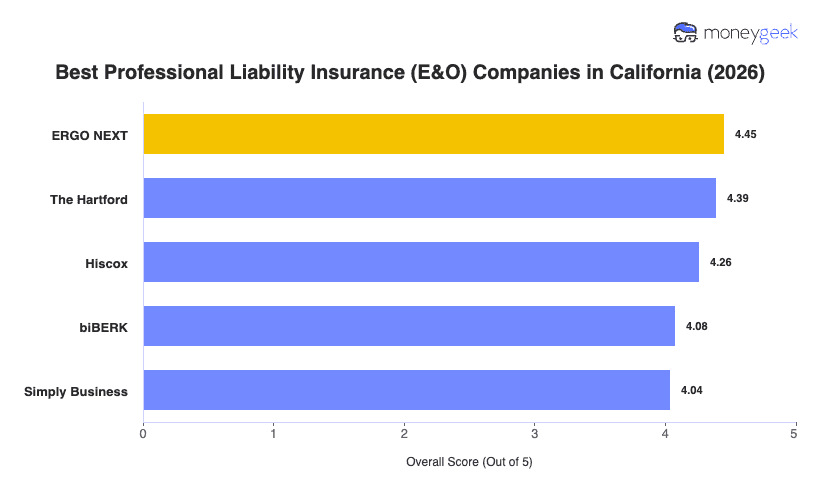

Our analysis of California professional liability insurers found three providers that consistently outperformed the field: ERGO NEXT, The Hartford and Hiscox each earned high marks across affordability, customer experience and coverage quality.

- ERGO NEXT: ERGO NEXT ranks first across 11 industries in California including healthcare, construction, fitness and pet care, giving it the broadest industry fit of any provider on this list. Its digital-first buying experience makes it easy to get covered quickly without going through a broker.

- The Hartford: The Hartford leads the field in consulting, education, financial services, hospitality and cleaning services in California, backed by dedicated specialist support teams that know these industries. Businesses that want hands-on claims guidance and profession-specific policy options will find it a strong fit.

- Hiscox: Hiscox ranks first for tech/IT businesses in California and places second in financial services, childcare, consulting and nonprofit sectors. Its policies are built for smaller professional firms and solo practitioners who need straightforward, profession-specific coverage without excess complexity.

These three providers suit most California businesses well, but no ranking captures every consideration your operation has. Comparing business insurance options side-by-side and getting direct quotes gives you the clearest picture of what fits your specific situation.