Drivers with no credit history have three immediate paths to a lower premium: telematics enrollment, multi-carrier quoting and credit building. Each works on a different timeline and produces a different size of savings.

Car Insurance With No Credit History

Updated: June 5, 2026

Advertising & Editorial Disclosure

Key Takeaways

Drivers without a credit history pay an average of $102 a month versus $58 for those with excellent credit, a gap of $44 a month or $528 a year.

Most states treat no credit history as its own pricing tier, separate from poor credit. California, Hawaii, Massachusetts, Michigan and Washington ban credit-based pricing altogether.

Comparing quotes from multiple insurers is the most direct way to find a lower rate. Some high-risk driver programs also place less weight on credit history.

How to Get Car Insurance With No Credit History

- 1Start with telematics or usage-based insurance

Telematics programs base rates on actual driving behavior rather than credit history. Progressive Snapshot, State Farm Drive Safe & Save and GEICO DriveEasy all offer this option. A driver with a clean record and no credit can earn lower premiums through these programs within the first policy term. Usage-based insurance charges a per-mile rate and is worth pricing out if you drive fewer than 7,500 miles a year.

- 2Get quotes from at least five carriers

The spread between the cheapest and most expensive insurer for a no-credit-history driver is $816 per year, as the rate table above shows. The pricing gap between carriers comes from how credit score affects car insurance rates, with each insurer weighing the absence of a credit file differently. Getting quotes from GEICO, Travelers, Nationwide, Progressive and at least one regional carrier gives you a realistic floor.

- 3Ask about credit-neutral discounts

Safe driver, low mileage, multi-policy and pay-in-full are all credit-neutral discounts that apply regardless of credit score. Ask each insurer to apply all eligible discounts before accepting a final quote. On a $102 monthly premium, a stacked 15% discount saves $184 a year without touching your credit file.

- 4Open a secured credit card

A secured credit card with a $200 to $500 limit, used for small purchases and paid in full monthly, produces a scoreable credit file. Reaching the fair tier drops your average monthly premium from $102 to $89, saving $156 per year. Reaching good drops it to $62 per month, saving $480 per year compared to having no credit file.

How Does Having No Credit History Affect Car Insurance Rates?

Insurers treat no credit history as a risk signal and price it higher than most credit tiers. Auto insurers use a credit-based insurance score, built from your credit report, to predict how likely you are to file a claim. Without any credit history, insurers can't generate that score and assign a higher rate as a result.

Drivers with no credit history pay $102 per month on average, versus $58 per month for drivers with excellent credit. That $44 monthly gap adds up to $528 per year. Reaching the fair credit tier drops the average to $89 per month, saving $13 per month. Reaching good credit drops it to $62 per month, saving $40 per month compared to having no credit file at all.

Credit Score Tier | Monthly Premium | Annual Premium |

|---|---|---|

No Credit History | $102 | $1,225 |

Poor | $147 | $1,759 |

Below Fair | $112 | $1,340 |

Fair | $89 | $1,070 |

Good | $62 | $740 |

Excellent | $58 | $697 |

Drivers with no credit history pay less on average than drivers with poor or below fair credit. A blank file shows less negative signal than a file with missed payments or collections on record.

How Much Does Car Insurance Cost by Company With No Credit History?

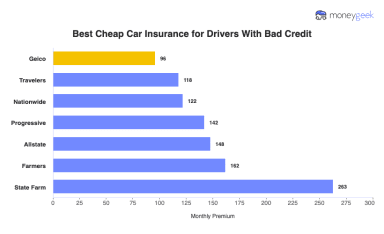

GEICO charges $68 per month for drivers with no credit history, the lowest rate among major national insurers. Allstate charges $136 per month for the same driver, the highest. That $68 monthly spread adds up to an $816 annual difference for an identical profile.

$68 | $96 | $64 | $45 | $42 | |

$97 | $122 | $94 | $72 | $65 | |

$99 | $118 | $75 | $51 | $46 | |

$107 | $142 | $100 | $69 | $63 | |

$108 | $263 | $93 | $51 | $40 | |

$133 | $162 | $111 | $81 | $75 | |

$136 | $148 | $111 | $82 | $84 |

Which States Don't Allow Credit Checks for Car Insurance?

Five states prohibit insurers from using credit history to set auto insurance rates: California, Hawaii, Massachusetts, Michigan and Washington. Drivers in these states pay rates based on driving record, age, vehicle type and location. Credit is not a factor.

If you live in one of these five states, your lack of credit history won't add a dollar to your premium. You still need to compare quotes because rates vary by insurer, but credit is off the table as a pricing factor. Drivers in all other states are subject to credit-based pricing unless their insurer is among those that opt out voluntarily.

No Credit History vs. Bad Credit: What's the Difference for Insurance?

No credit history and bad credit produce different insurance outcomes, and the rate data confirms this. Drivers with no credit history pay $102 per month on average, while drivers with poor credit pay $147 per month. A blank file carries less negative signal than a file with missed payments or derogatory marks.

A driver with no credit history has no negative marks to wait out and can reach a better rate tier faster. Drivers repairing bad credit may need years to clear derogatory marks, and the timeline depends on what's on the file. Both can reduce their rate by enrolling in telematics programs, which reward safe driving regardless of credit score.

How to Build Credit to Lower Your Car Insurance Rate

Moving from no credit history to the good tier cuts the average monthly premium by $40, saving $480 per year at renewal. The steps below build a scoreable file and move you into a lower rate tier. Once your credit improves, re-quoting is essential — your current insurer won't automatically apply the new tier, and you can cut your rate further by shopping at renewal.

Pay all bills on or before the due dates. Payment history is the largest component of a credit score, and a single missed payment can delay your progress by months. Set up automatic payments for the minimum due on any accounts, then pay the full balance separately before the due date.

Keep your credit utilization below 30% of your available limit. If you open a secured card with a $300 limit, keep the reported balance under $90. Pay down the balance before your statement closes, since credit bureaus report balances as of the statement date. Don't open multiple new accounts at once. Several hard inquiries in a short window can reduce your score even while your payment history improves.

Car Insurance With No Credit History: Bottom Line

Drivers with no credit history pay an average of $102 per month. GEICO offers the lowest rate at $68 per month, while Allstate charges $136. Compare quotes from at least five carriers, apply for telematics discounts and start building credit. Reaching the good credit tier drops your average monthly premium to $62, and comparing those new quotes against the lowest full coverage rates nationally at renewal is the step most drivers skip.

No Credit History Auto Insurance: FAQ

Can I get car insurance with no credit history?

Yes. All major insurers write policies for drivers with no credit history. You'll pay a higher rate, with the average at $102 per month for full coverage, but coverage is available. Telematics programs from Progressive, State Farm and GEICO offer pricing based on driving behavior rather than credit score, which can reduce your premium from the first renewal.

Which insurance companies are cheapest for drivers with no credit history?

GEICO charges $68 per month for drivers with no credit history, the lowest among major carriers in this analysis. Nationwide and Travelers follow at $97 and $99 per month. Allstate charges $136 per month for the same profile. Getting at least five quotes is the only reliable way to find your actual floor, since rates vary by state, vehicle and coverage level.

Do all states allow insurers to use credit history for pricing?

No. California, Hawaii, Massachusetts, Michigan and Washington prohibit auto insurers from using credit history as a pricing factor. Drivers in these five states pay rates based on driving record, location, age and vehicle. If you live in one of these states, your lack of credit history has no impact on your auto insurance premium.

How can I lower my car insurance rate without a credit history?

Compare quotes from multiple carriers and apply for credit-neutral discounts such as safe driver, low mileage and pay-in-full. Enrolling in a telematics program is also worth doing if you have a clean driving record. Building even a thin credit file moves you into a lower rate tier and cuts your average monthly premium.

Does no credit history affect car insurance differently than bad credit?

Yes. Drivers with no credit history pay an average of $102 per month, while those with poor credit pay $147 per month. A blank file carries less negative signal than one with missed payments or collections. The path to a lower rate is faster from a blank file, since there are no derogatory marks to wait out.

MoneyGeek sourced rate data from Quadrant Information Services, which provides quote information that isolates each major factor influencing car insurance premiums across all residential ZIP codes in the U.S. Our base profile for this analysis:

- Single 40-year-old male

- 2012 Toyota Camry LE

- Clean driving record

- No claims history

- Valid U.S. driver's license

- Full coverage: 100/300/100 liability with a $1,000 deductible for comprehensive and collision

Rates were segmented by credit score tier, including a dedicated no-credit-history profile for drivers with no scoreable credit file. Credit tiers represented are No Credit History, Poor, Fair, Good and Excellent. Company-level rates reflect averages across multiple ZIP codes to reduce geographic distortion. All figures are rounded to whole dollars. A few important limitations to note:

Credit-based insurance scoring is prohibited in California, Hawaii, Massachusetts and Michigan. Rates in those states are not influenced by credit tier. Each driver's actual rate depends on their unique profile. The figures on this page are averages and your quotes may differ. MoneyGeek receives monthly data refreshes from Quadrant Information Services to keep rate information current. Insurance regulations vary by state. Always verify coverage requirements with your state's insurance department. For a full explanation of how MoneyGeek collects and presents insurance data, see our auto insurance methodology.

About Mark Fitzpatrick

Mark Fitzpatrick, a Licensed Property and Casualty (P&C) Insurance Producer in Connecticut, is MoneyGeek's resident insurance expert. He has spent nearly a decade analyzing the market, first at LendingTree and now at MoneyGeek, where he produces original research on hundreds of carriers and millions of rates across auto, home, renters, health and life insurance.

He covers economics and insurance at MoneyGeek, and his work has been featured in The Washington Post, The New York Times and NPR, among other outlets.

Like all MoneyGeek analysts, he draws on independent cost and consumer experience data. No insurance company partnership influences his recommendations.

Fitzpatrick earned his degrees from Johns Hopkins University (M.A. Economics and International Relations) and Boston College (B.A.). His career began in financial risk management at State Street. He's also a five-time “Jeopardy!” champion.