Insurance

Insurance helps protect your health, property, income and future. Learn how the different coverage types work to choose the right policy for your needs.

Advertising & Editorial Disclosure

What Is Insurance?

Insurance is a financial tool that protects policyholders and their assets from unexpected losses. When you buy a policy, you enter an agreement with an insurer to cover risks such as accidents, damage or liability in exchange for a premium. Insurance provides a financial safety net after unexpected events. The right coverage limits your out-of-pocket costs after a car accident or medical emergency. It won't prevent those events, but it reduces the financial damage when they happen.

Premium

PremiumThis is the amount you pay to keep your insurance policy active, usually billed monthly or annually, regardless of whether you file a claim.

Deductible

DeductibleThis is a fixed amount you must pay out of pocket before your insurance covers remaining eligible costs. Higher deductibles often result in lower premium payments.

Coverage Limit

Coverage LimitThe maximum amount your insurer will pay for a covered claim is called the coverage limit. If your expenses exceed this limit, you’re responsible for the remaining costs.

Claim

ClaimA claim is a formal request submitted to your insurance company asking for payment based on the terms of your policy after a covered event occurs.

Policy

PolicyThis written agreement between you and your insurer outlines the coverage details, exclusions, premium costs, deductibles and rules that govern your protection.

Insurer

InsurerThis refers to the company providing the insurance policy. The insurer assumes the financial risk in exchange for premium payments.

Exclusions

ExclusionsThese are situations or events not covered by an insurance policy. Common exclusions include intentional damage, wear and tear, and certain high-risk activities.

Copay

CopayPrimarily used in health insurance, a copay is a fixed amount the insured pays for certain services, such as doctor visits and prescriptions. Your insurance covers the remaining eligible costs.

Insurance Basics: Understanding the Types of Insurance

Find the Best Insurance Companies: Our Top Picks by Category

Car Insurance

Car insurance offers financial protection in case your vehicle is damaged, stolen or involved in an accident. It typically includes coverage for liability, collision and comprehensive risks, and some policies offer additional options like roadside assistance or rental reimbursement. In most states, drivers must carry at least a minimum amount of liability coverage to legally operate a vehicle. Understanding your auto insurance options helps ensure you get the right protection at a price that fits your budget.

Home Insurance

Your home is likely one of the biggest financial investments you’ll ever make — and protecting it with the right insurance matters. Home insurance helps cover repair or rebuilding costs after damage from events like fires, storms or theft. It can also protect your belongings and provide personal liability coverage if someone gets injured on your property.

Renters Insurance

If you rent your home or apartment, renters insurance offers an affordable way to protect your personal belongings from damage or theft. While your landlord’s policy covers the building, it doesn’t extend to your furniture, electronics or other valuables. Renters insurance can also include personal liability coverage, which may protect you if someone gets injured in your home — or even if your pet causes damage. Understanding what’s covered, how much renters policies cost and how much protection you need can help you choose the right coverage without overspending.

Life Insurance

Life insurance provides a death benefit that can cover funeral costs, replace lost income or help pay off debts. Beyond basic protection, certain types of life insurance policies, like whole or universal also serve as long-term financial tools.

Health Insurance

Health insurance helps you access medical care. Whether you’re insured through your employer, the state Marketplace or a government program like Medicare or Medicaid, understanding your health insurance options can help you make an informed decision. Learn about how plans work including premiums, deductibles and provider networks

Small Business Insurance

Small business insurance coverage ensures operations can continue after unforeseen events. The right policy protects your assets, covers legal costs and helps you meet regulatory or contract requirements. Compare small business insurance coverage types that are most commonly needed and guides to help you below.

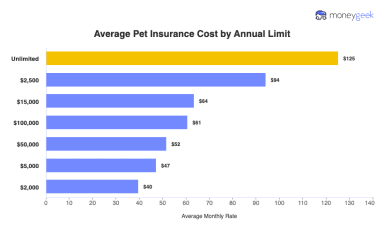

Pet Insurance

Pet insurance helps cover the cost of veterinary care in the event of accidents, illnesses or emergencies, and for some pet owners, it can mean the difference between life-saving treatment and financial strain. While not every policy is the right fit for every pet, it can be particularly valuable for breeds prone to health issues or for owners seeking more predictable care costs. Unlike human health insurance, pet insurance isn’t heavily regulated, which means coverage and exclusions vary widely.