Toyota Camry insurance costs average $90 monthly for minimum coverage and $175 for full coverage. But, depending on your specific trim and model year, costs can range from $59 for a 2004 Toyota Camry to $291 for a 2016 Toyota Camry monthly.

Toyota Camry Insurance Cost

Key Takeaways

Toyota Camry insurance costs range from $89 to $291 monthly, with significant variation based on specific trim level and model year you choose.

The Camry ranks 373rd out of 827 vehicle models for insurance affordability in the 2025 United States auto market, placing it in the middle tier.

GEICO provides the most affordable Toyota Camry insurance with full coverage starting at $131 per month and minimum coverage policies beginning at $61 monthly.

How Much Is Toyota Camry Insurance?

| Toyota Camry | $90 | $175 |

Your Next Step:

Get your real quotes from trusted insurance providers.

Toyota Camry Insurance Cost by Model Year

Your Toyota Camry's model year and available trims directly impact insurance rates. Newer models cost more to insure because of their higher fair value. Monthly premiums for Camry models range from $65 to $250, with older vehicles generally offering the most affordable coverage options.

| 2025 | $106 | $206 |

| 2024 | $102 | $197 |

| 2023 | $100 | $194 |

| 2022 | $92 | $178 |

| 2021 | $82 | $158 |

| 2020 | $93 | $180 |

| 2019 | $94 | $182 |

| 2018 | $93 | $179 |

| 2017 | $87 | $168 |

| 2016 | $129 | $250 |

| 2015 | $113 | $219 |

| 2014 | $100 | $194 |

| 2013 | $90 | $174 |

| 2012 | $85 | $165 |

| 2011 | $73 | $141 |

| 2010 | $69 | $133 |

| 2009 | $92 | $177 |

| 2008 | $84 | $161 |

| 2007 | $74 | $142 |

| 2006 | $72 | $139 |

| 2005 | $65 | $125 |

| 2004 | $68 | $130 |

| 2003 | $68 | $131 |

| 2002 | $71 | $136 |

| 2001 | $66 | $127 |

| 2000 | $73 | $140 |

Your Next Step:

Get your real quotes from trusted insurance providers.

Toyota Camry Insurance Cost by Trim

Your Toyota Camry's trim affects insurance costs based on features, rarity and market value. Our research shows monthly premiums vary widely by trim, ranging from $71 for basic models to $259 for premium variants like hybrid editions.

| Ce Sedan 4d | $71 | $137 |

| Sedan 4d | $73 | $140 |

| Hybrid Sedan 4d | $75 | $145 |

| Le Sedan 4d | $82 | $159 |

| Le Hybrid Sedan 4d | $87 | $168 |

| Se Sedan 4d | $88 | $169 |

| Xle Sedan 4d | $89 | $171 |

| Xle Hybrid Sedan 4d | $89 | $173 |

| Se Nightshade Edition Sedan 4d | $91 | $176 |

| L Sedan 4d | $92 | $177 |

| Le | $92 | $180 |

| Se Sport Sedan 4d | $96 | $186 |

| Trd Sedan 4d | $98 | $190 |

| Se | $98 | $191 |

| Xse Sedan 4d | $99 | $192 |

| Se Nightshade Edition | $101 | $195 |

| Gas | $109 | $210 |

| Xle | $109 | $211 |

| Xse | $111 | $215 |

| Trd | $111 | $216 |

| Hybrid Le Sedan 4d | $112 | $217 |

| Hybrid Xle Sedan 4d | $118 | $229 |

| Se Special Edition Sedan 4d | $125 | $243 |

| Hybrid Se Sedan 4d | $134 | $259 |

Your Next Step:

Get your real quotes from trusted insurance providers.

Does Upgrading Your Trim Increase Toyota Camry Insurance Costs?

Moving from the base CE up through the SE and XLE trims adds roughly $30–55 a month to a full coverage premium — not nothing, but rarely a dealbreaker when you're already comparing trims that differ by thousands in sticker price.

The exception is the hybrid lineup. Hybrid variants consistently cost more to insure than their gas equivalents at the same trim level, and the Hybrid SE tops out at $259/month — $122 more than the base CE.

If you're weighing a hybrid upgrade primarily for fuel savings, factor that insurance gap into the math before you decide.

Toyota Camry Insurance Cost by Company

Toyota Camry insurance costs vary by provider from $96 to $232 monthly. Minimum coverage ranges from $61 to $159, while full coverage costs $131 to $331. Each insurer uses different factors to calculate rates, which explains the price differences.

| GEICO | $61 | $131 |

| Travelers | $76 | $139 |

| State Farm | $84 | $174 |

| Progressive | $92 | $172 |

| Kemper | $96 | $193 |

| The Hartford | $97 | $166 |

| Nationwide | $100 | $172 |

| AAA | $103 | $217 |

| Amica | $111 | $226 |

| Allstate | $114 | $221 |

| Chubb | $118 | $240 |

| AIG | $133 | $331 |

| Farmers | $137 | $242 |

| UAIC | $159 | $198 |

Your Next Step:

Get your real quotes from trusted insurance providers.

Toyota Camry Insurance Cost by State

Toyota Camry insurance costs vary by location, ranging from $31 monthly in Wyoming to $375 in Louisiana.

| Alabama | $77 | $145 |

| Alaska | $62 | $132 |

| Arizona | $109 | $203 |

| Arkansas | $71 | $158 |

| California | $87 | $178 |

| Colorado | $85 | $203 |

| Connecticut | $125 | $214 |

| Delaware | $130 | $218 |

| District Of Columbia | $107 | $199 |

| Florida | $131 | $304 |

| Georgia | $132 | $217 |

| Hawaii | $47 | $105 |

| Idaho | $48 | $97 |

| Illinois | $79 | $148 |

| Indiana | $57 | $112 |

| Iowa | $49 | $118 |

| Kansas | $63 | $147 |

| Kentucky | $109 | $184 |

| Louisiana | $174 | $375 |

| Maine | $45 | $94 |

| Maryland | $138 | $233 |

| Massachusetts | $88 | $187 |

| Michigan | $136 | $260 |

| Minnesota | $74 | $153 |

| Mississippi | $78 | $153 |

| Missouri | $103 | $205 |

| Montana | $62 | $146 |

| Nebraska | $66 | $149 |

| Nevada | $159 | $288 |

| New Hampshire | $62 | $109 |

| New Jersey | $155 | $254 |

| New Mexico | $71 | $159 |

| New York | $119 | $212 |

| North Carolina | $74 | $146 |

| North Dakota | $52 | $114 |

| Ohio | $65 | $126 |

| Oklahoma | $82 | $182 |

| Oregon | $105 | $183 |

| Pennsylvania | $83 | $195 |

| Rhode Island | $108 | $193 |

| South Carolina | $91 | $170 |

| South Dakota | $46 | $141 |

| Tennessee | $68 | $138 |

| Texas | $111 | $228 |

| Utah | $98 | $166 |

| Vermont | $39 | $93 |

| Virginia | $84 | $136 |

| Washington | $82 | $153 |

| West Virginia | $77 | $155 |

| Wisconsin | $57 | $126 |

| Wyoming | $31 | $97 |

Your Next Step:

Get your real quotes from trusted insurance providers.

Toyota Camry Insurance Cost by Driver Profile

Your age and driving record impact your Toyota Camry insurance rates. Rates average $336 per month for drivers under 25 with clean records and drop to $132 for drivers aged 26 to 64.

| Adult Drivers | $90 | $175 |

| Young Drivers | $231 | $442 |

| Senior Drivers | $120 | $221 |

| Drivers With a Speeding Ticket | $112 | $219 |

| Drivers With an Accident | $133 | $256 |

| Drivers With a DUI | $165 | $315 |

| Drivers With Bad Credit | $213 | $428 |

Your Next Step:

Get your real quotes from trusted insurance providers.

Is a Toyota Camry Expensive to Insure?

Compared to the rest of the models on the U.S. market, a Toyota Camry ranks 373rd out of 827, making it one of the moderately expensive cars to insure. Among midsize sedans, the model ranks 30th out of 37.

| Saturn S-Series | $47 | $90 |

| Dodge Stratus | $52 | $100 |

| Saab 9-5 | $53 | $103 |

| Saturn L-Series | $56 | $107 |

| Pontiac Grand Am | $59 | $113 |

| Mercury Milan | $62 | $118 |

| Mercury Sable | $64 | $122 |

| Suzuki Verona | $68 | $130 |

| Chrysler Sebring | $68 | $130 |

| Saab 9-3 | $68 | $131 |

| Mercury Montego | $71 | $137 |

| Pontiac Grand Prix | $73 | $140 |

| Pontiac G6 | $75 | $144 |

| Mitsubishi Galant | $76 | $146 |

| Chevrolet Malibu | $78 | $151 |

| Ford Fusion | $80 | $155 |

| Nissan Altima | $80 | $155 |

| Volkswagen CC | $81 | $156 |

| Nissan Maxima | $82 | $159 |

| Volkswagen Passat | $83 | $159 |

| Hyundai Azera | $84 | $162 |

| Honda Clarity | $85 | $164 |

| Dodge Magnum | $85 | $164 |

| Subaru Legacy | $85 | $165 |

| Honda Accord | $86 | $166 |

| Chrysler 200 | $86 | $166 |

| Mazda 6 | $86 | $167 |

| Dodge Avenger | $87 | $168 |

| Kia Optima | $89 | $172 |

| Toyota Camry | $90 | $175 |

| Hyundai Sonata | $96 | $186 |

| Hyundai Ioniq 6 | $96 | $187 |

| Kia K5 | $99 | $193 |

| Toyota Crown | $108 | $210 |

| Kia Stinger | $121 | $235 |

| Toyota Mirai | $140 | $273 |

| Lucid Air | $160 | $314 |

Your Next Step:

Get your real quotes from trusted insurance providers.

Factors That Affect Toyota Car Insurance Costs

Several factors affect what you'll pay for Toyota Camry insurance coverage:

Average Repair or Replacement Costs

Average Repair or Replacement CostsToyota ranks first in repair affordability among 59 U.S. automakers with median annual costs of $478. Toyota Camry repair costs average $577 annually, making it one of Toyota's most affordable models for repairs.

Vehicle Trim, Features and Accessories

Vehicle Trim, Features and AccessoriesThe Toyota Camry's moderate performance capabilities (203 to 208 horsepower, 0 to 60 mph in 7.6 seconds) keep insurance premiums reasonable compared to high-performance sedans.

Higher trim levels like XSE cost more to insure due to advanced features, 19-inch wheels and premium materials. The sportier XSE includes performance styling and larger wheels that can raise repair expenses after accidents.

Fuel Type

Fuel TypeToyota Camry costs less to insure because it runs on regular gasoline with proven, reliable engines. When something breaks, you can take it to any mechanic in the country. Parts are widely available and affordable.

The Camry hybrid models carry slightly higher insurance costs due to the battery system and electric motor complexity. But, Toyota's hybrid technology is well-established with 20+ years of market presence, so repair costs remain reasonable compared to newer electric vehicles.

Location

LocationToyota Camry owners are distributed nationwide with strong concentrations in California, Florida and Texas. The Camry ranks as the most popular car in Florida and holds strong positions across the Southern and Southwestern states, where Toyota has extensive dealer networks.

California leads with 172 Toyota dealerships, while Southeast Toyota (Alabama, Florida, Georgia, North Carolina and South Carolina) handles 24% of all U.S. Toyota sales. This distribution means competitive insurance rates nationwide, as insurers have extensive data on repair costs and claim patterns across all regions.

Driver Profile

Driver ProfileMost Toyota Camry drivers are middle-aged (average 49 years) with household incomes of $70,000 to $90,000. This demographic receives moderate insurance rates due to established credit histories and stable driving patterns.

Driver demographics affect Camry insurance rates:

- Age (average 49 years): Middle-aged drivers receive lower rates than younger buyers due to driving experience and stability.

- Gender (50% male, 50% female): Toyota has the most balanced gender distribution among major automakers, reflecting broad market appeal.

- Income ($70,000 to $90,000 average): Middle-class income levels correlate with responsible driving behaviors and steady premium payments.

The Camry attracts family-focused, safety-conscious drivers who prioritize reliability over performance, creating a lower-risk insurance profile that results in competitive rates.

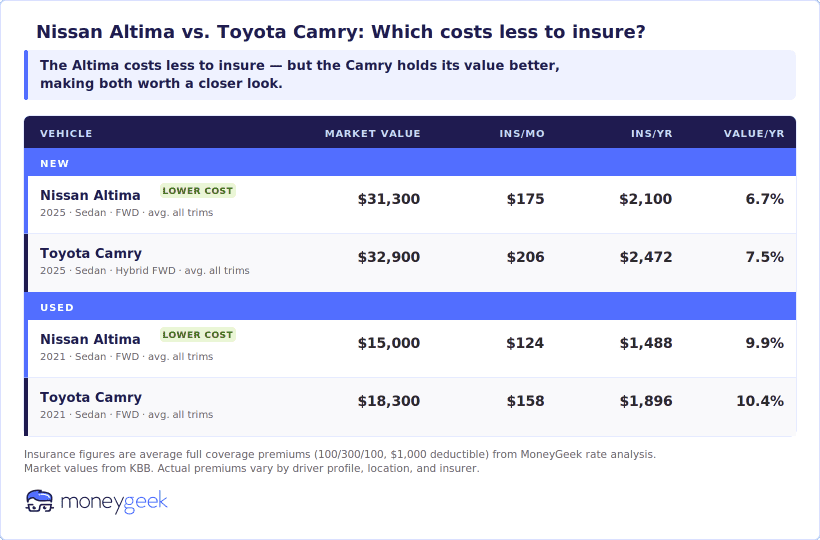

Toyota Camry vs. Nissan Altima: Which Is Cheaper to Own?

Among midsize sedans, few matchups are more common than the Camry versus the Altima. Both sit at the top of the class in sales, and buyers who haven't committed to a brand almost always end up comparing these two.

On insurance, the Altima has a clear edge. Full coverage on a 2025 Altima runs $31 less per month than a 2025 Camry — that's $372 back in your pocket each year. Used buyers see the same pattern — a 2021 Altima costs $34 less per month to insure than a 2021 Camry.

Where the Camry earns its premium is resale value and fuel economy. A 2021 Camry holds roughly $3,300 more in value than a similar Altima, and the 2025 Camry's hybrid powertrain delivers 51 mpg against the Altima's 32 — a gap wide enough to offset the insurance difference over time.

Taken together, the two cars cost about the same to own relative to what you pay for them. The Altima favors buyers focused on keeping monthly costs low. The Camry rewards those thinking longer term — fuel savings, stronger resale, and total cost of ownership.

How to Lower the Cost of Toyota Camry Insurance

Five ways to lower your Toyota Camry insurance costs:

- 1Choose the right coverage

How much coverage you need for your Toyota depends on its value, how often you drive and what your budget can actually support. You can keep it minimal with state liability and a $1,000 deductible or move to 100/300/100 with a $500 deductible, and lenders may require gap insurance if you are financing or leasing.

- 2Research costs and companies

Compare average auto insurance costs for your car to see how much you're saving. Look for the cheapest car insurance companies in your area.

- 3Look beyond low rates

To get the most balanced car insurance, check forum reviews, J.D. Power customer satisfaction scores, Better Business Bureau complaint records and AM Best financial strength ratings while comparing coverage limits and deductibles. Some low-cost insurers have slower claim processing or limited coverage options that leave you underinsured in an accident.

- 4Explore discounts you qualify for

Toyota Camry owners can lower their insurance costs by using discounts tied to multi-vehicle households, bundled policies, clean driving records, strong safety ratings and good student eligibility. Since many Camry drivers are families, responsible commuters and students who benefit from the car’s top-tier safety features, these savings tend to stack easily and drive premiums down.

- 5Consider alternative car insurance types

Toyota Camry owners should explore Toyota Insurance (if available in your area) for vehicle-specific coverage and competitive rates, or usage-based insurance programs like USAA SafePilot that reward safe driving with lower premiums.

- 6Check rates annually

Comparing car insurance quotes from multiple sources can help you save up to 24% on your Toyota Camry insurance. Your best deal today might not exist next year, so compare rates annually.

Toyota Camry Insurance Cost: Bottom Line

Insuring a Toyota Camry costs more than average, but you can still find decent rates. Shop multiple companies, look into discounts and consider different coverage options to get the best insurance rate for your car.

Toyota Camry Insurance Rates: FAQ

Here are answers to common questions about insuring a Toyota Camry.

The Toyota Camry's average annual insurance cost is $1,083 yearly for state minimum and $2,095 for full coverage.

GEICO offers the cheapest minimum coverage and full coverage car insurance for Toyota Camrys, with annual rates of $732 and $1,572, respectively.

Toyota Camry insurance is moderately more expensive than most cars. Out of 827 vehicles we track, the Camry ranks 373rd for affordability. Among midsize sedans, this model sits at 30th out of 37.

Several things drive up your Toyota Camry rates. Repairs cost more because of specialized parts. Your driving record and credit score, plus the coverage you pick, play a big role. Where you live affects rates, too. Areas with more theft or weather-related risks will cost more.

Shop around with multiple insurers as rates vary for Toyotas, and consider usage-based insurance programs that track your driving habits. Take advantage of Toyota Camry's safety features when discussing discounts, bundle with other policies and maintain a clean driving record to qualify for the lowest premiums.

How We Determined Toyota Camry Insurance Costs

We studied hundreds of millions of quote estimates across all U.S. models sold in the U.S. from 2000 to 2025 to get you the most accurate Toyota Camry insurance costs.

Who We Based These Rates On

These Toyota Camry prices reflect what a typical driver pays:

- Age 40, unmarried male

- Clean record: no tickets or crashes

- Credit score in a good range

- Has never made an insurance claim

- Puts about 12,000 miles on the odometer yearly

- Has a valid driver's license with no suspensions on record

Coverage Definitions:

- Minimum Coverage: State-required liability limits

- Full Coverage: 100/300/100 liability + comprehensive/collision with $1,000 deductibles

About Mark Fitzpatrick

Mark Fitzpatrick, a licensed Property and Casualty (P&C) Insurance Producer in Connecticut, is MoneyGeek's resident expert in insurance and economics. He has spent nearly a decade covering the market, first at LendingTree and now at MoneyGeek, where he analyzes hundreds of carriers and millions of rates across auto, home, renters, health and life insurance.

His work has appeared in The Washington Post, The New York Times and NPR. He draws on independent cost and consumer experience data, and no insurance company partnerships influence his recommendations.

Mark studied at Boston College before earning a master's in economics and international relations from Johns Hopkins University. Before MoneyGeek, he worked in financial risk management at State Street. He's also a five-time “Jeopardy!” champion.