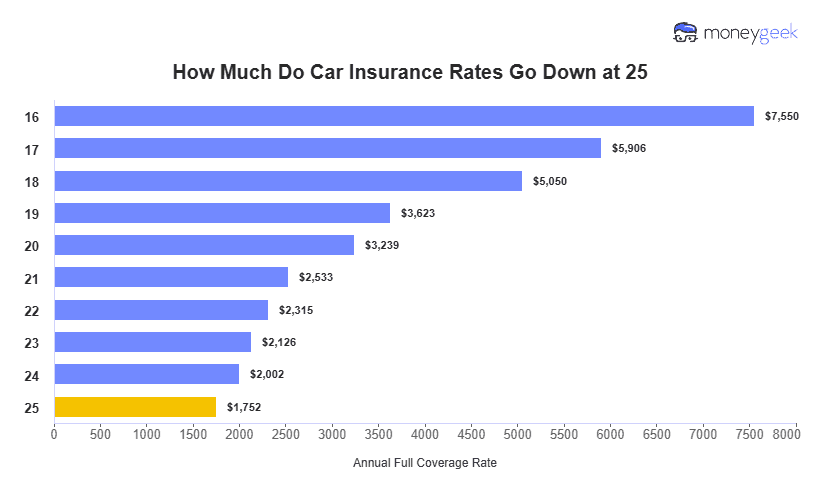

The average car insurance at age 25 costs $146 per month, or $1,752 per year, for full coverage with 100/300/100 liability limits — $21 per month less than at 24. Insurers price 25-year-olds as lower risk than younger drivers, but your driving record and credit history still shape your final premium.

Full coverage averages $7,550 per year at 16 and $2,533 per year at 21. By 25, it's $1,752, a 77% drop from the teenage peak. Most of those savings come before 25, and reductions after that age are smaller each year.