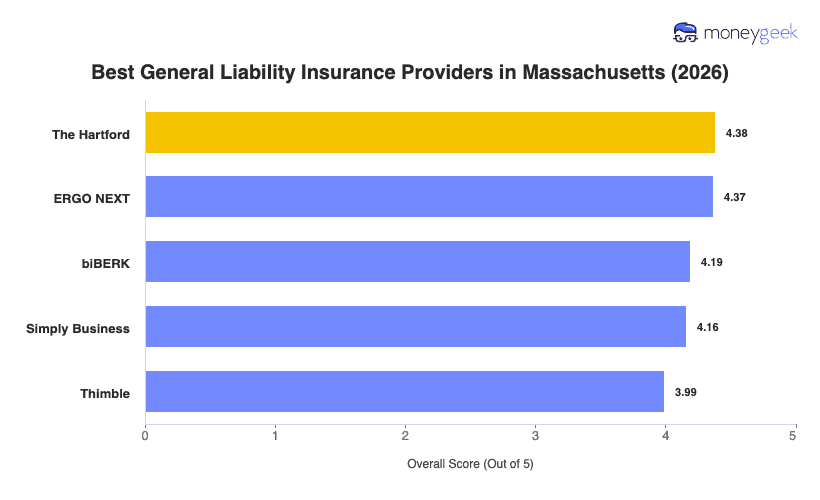

A Worcester manufacturer, Cape Ann fishing operation and Framingham retail shop each need different coverage approaches. We found the five best general liability insurance companies in Massachusetts from out analysis that ranked them for pricing strength, customer support quality and coverage breadth:

- The Hartford: Best Overall, Best for Professional Services

- ERGO NEXT: Best for Customer Experience

- biBerk: Best for Lower-Risk Service Businesses

- Simply Business: Best for Comparing Carriers

- Thimble: Best for On-Demand Coverage

These providers cover the range of risks Massachusetts businesses deal with, from slip-and-fall claims in storefront operations to equipment damage during nor'easters. The profiles below explain what each insurer does well and which business types get the most value.