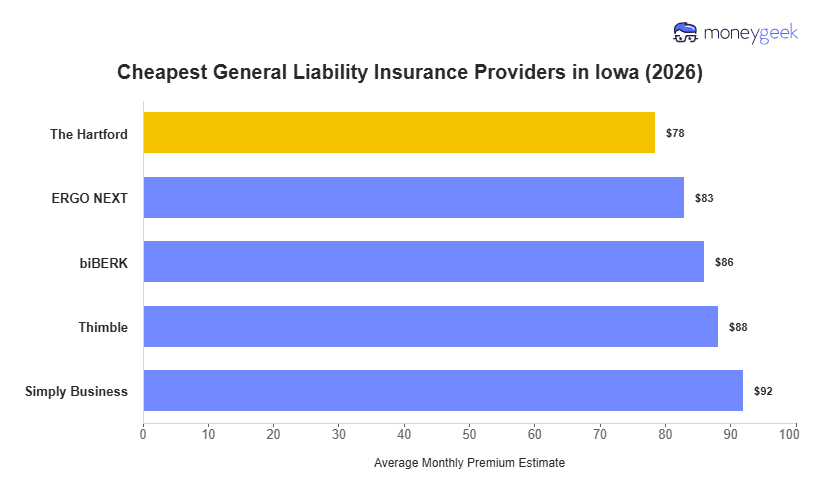

The cheapest general liability insurance companies in Iowa vary by industry, with different insurers offering the lowest rates depending on your type of business.

- The Hartford: Often cheapest for office-based professional services and community-focused businesses (arts and media companies, financial services firms, marketing and communications agencies, nonprofit organizations)

- ERGO NEXT: Generally has the lowest rates for hands-on trades and service businesses (construction and contracting, repair and maintenance services, manufacturing operations)

- biBERK: Typically most affordable for personal services and property-related businesses (cleaning services, fitness centers, pet care providers, real estate and property services, recreation and sports facilities)

- Simply Business: Usually cheapest for retail, technology, and childcare operations

>> Click each provider to learn more

These categories serve as a starting point for identifying which insurers to compare. Your actual rate will vary based on your specific business activities, revenue, location within Iowa, and coverage limits, so request quotes from the providers that match your business type to find your lowest price.