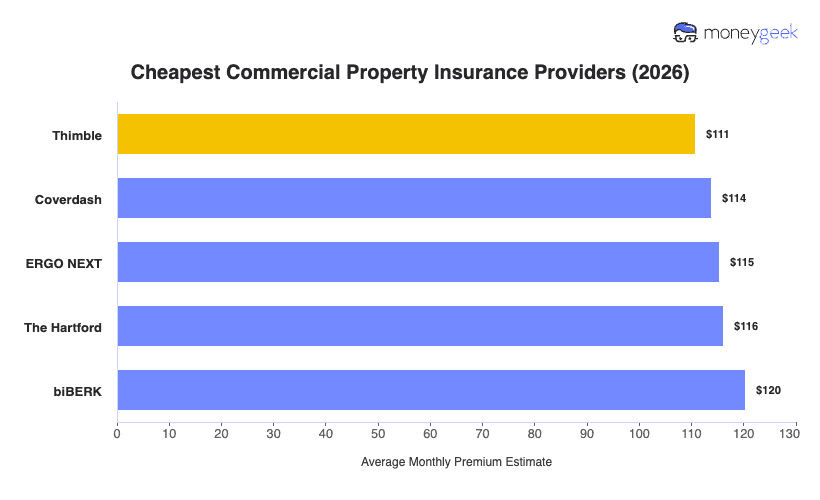

Below are the three cheapest commercial property insurance providers in MoneyGeek's analysis:

- Thimble: At $111 per month, Thimble prices 11% below the national average and holds the top overall affordability rank in MoneyGeek's analysis. It prices most competitively in the Southeast and Appalachian states, and is the cheapest option for businesses in Alabama, Arkansas, Georgia, Kentucky, Mississippi, South Carolina, Tennessee and West Virginia.

- Coverdash: Averaging $114 per month, it prices 9% below the national average and leads in 12 Northeast and mid-Atlantic states, including New York, New Jersey, Massachusetts, Connecticut and Pennsylvania. It's the strongest option for businesses operating in that region.

- ERGO NEXT: With the widest industry and state footprint of the three, it averages $115 per month, 8% below the national average, and prices lowest in 10 of 25 general industries and 31 of 51 states and territories in MoneyGeek's analysis.

These top three picks are not the lowest-cost option for every business. Your commercial property insurance costs will vary by industry, number of employees, property location and coverage limits selected. Use these rankings as a starting point and compare quotes for your specific profile.