The right general liability coverage depends on your business. We evaluated 10 major insurers across 408 business types in Iowa to identify the best and cheapest providers for small businesses. These five balance competitive pricing, reliable service and flexible coverage options.

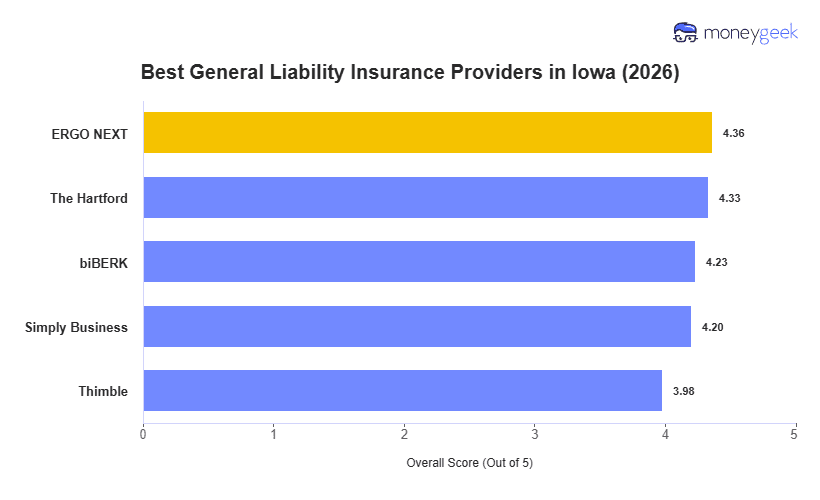

- ERGO NEXT: Best Overall, Best for Digital-First Businesses

- The Hartford: Best for Professional And Regulated Industries

- biBerk: Best for Service and Recreation Businesses

- Simply Business: Best for Comparing Carrier Options

- Thimble: Best for On-Demand Coverage

From a family-owned farm supply store in Sioux City to a growing landscaping crew in the Quad Cities, Iowa small businesses have distinct coverage needs. The table below shows each provider's rates and rankings, so you can match the right policy to your operations and budget.