Manufacturing plants, farm equipment dealers and health care providers drive Indiana's economy, and each faces different liability exposures. Finding the best general liability insurance means matching coverage to your specific operations, not just picking the cheapest policy. These five insurers balance cost with service quality and coverage flexibility:

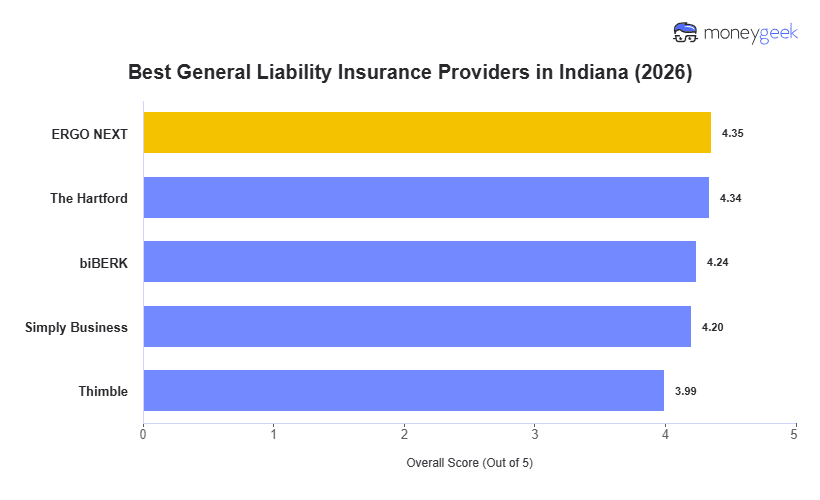

- ERGO NEXT: Best Overall, Best for Very Small Businesses in Hands-On Industries

- The Hartford: Best Cheap General Liability Insurance

- biBerk: Best for Service-Oriented Businesses

- Simply Business: Best for Comparing Carriers

- Thimble: Best for On-Demand Coverage

An auto repair shop in South Bend needs different protection than a consulting firm in Fishers or a cleaning service in Evansville. Here's what distinguishes each provider: