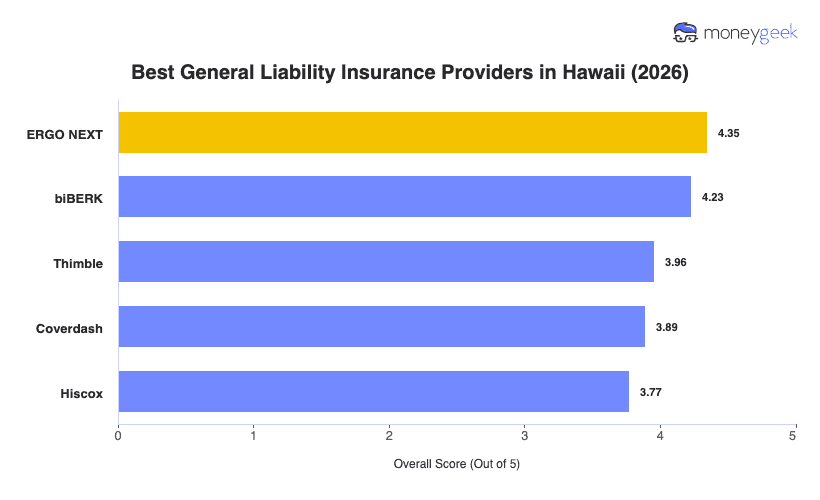

Small businesses in Hawaii have distinct coverage needs, whether running tours or operating a storefront. After analyzing 10 general liability insurers at $1 million per occurrence/$2 million aggregate limits, these five ranked as the best and most affordable options for local businesses.

- ERGO NEXT: Best Overall, Best for Tourism and Service Industries

- biBerk: Best for Health Care and Fitness Industries

- Thimble: Best for Short-Term and Project-Based Coverage

- Coverdash: Best for Coverage Options

- Hiscox: Best for Financial Services

Whether you operate a food truck in Kailua or manage a landscaping crew on the Big Island, the table below shows each provider's rates and rankings. Your ideal match may shift based on coverage needs and budget, so review the details to compare.