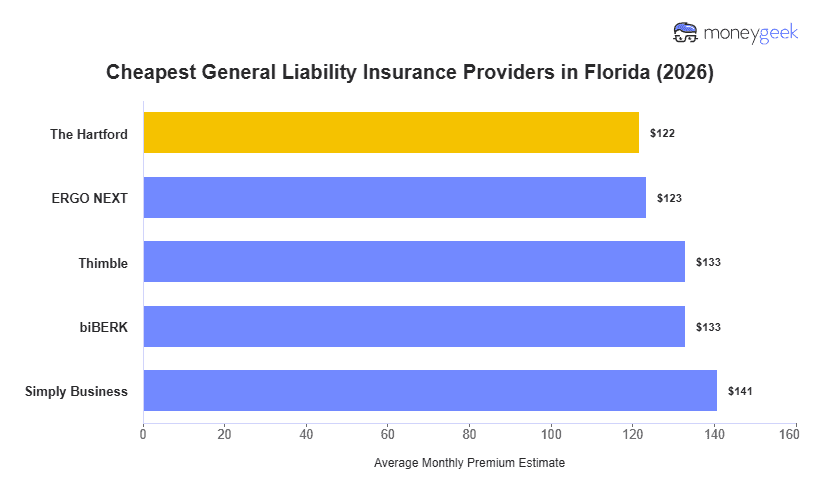

Across 25 general industries, The Hartford, NEXT and biBerk consistently offer the cheapest general liability insurance in Florida, though which one costs least depends on your specific business type and operations.

- The Hartford: Most affordable for professional services and creative businesses (IT consultants, financial advisors, photographers, web developers)

- ERGO NEXT: Lowest rates for hands-on trades and personal care services (carpentry, plumbing, hair salons, massage therapy)

- biBerk: Cheapest for fitness centers and cleaning companies (bowling alleys, gyms, janitorial services, carpet cleaning)

[Click Each Provider to Learn More]

Your final premium reflects your industry's risk profile, annual revenue, team size and claims history. A Miami wedding photographer faces different exposure than a Tampa roofing contractor or an Orlando cleaning service, so treat these patterns as your research starting point and compare quotes from all three carriers to find your actual lowest price.