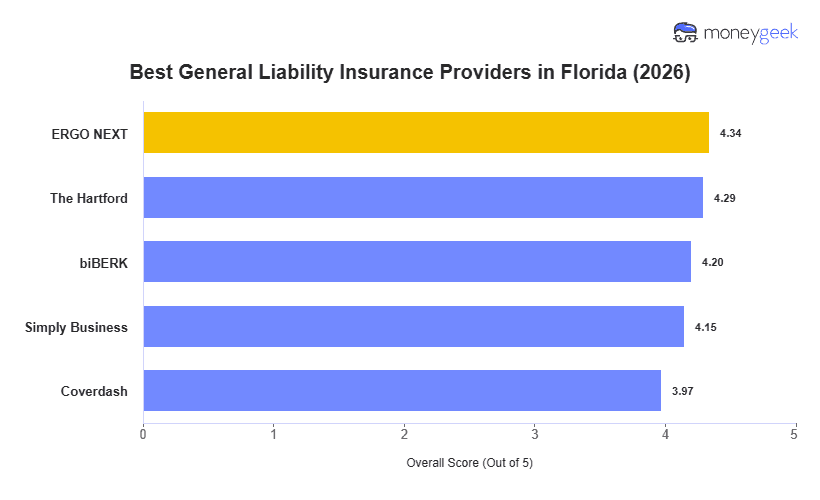

The best general liability insurance options for Florida small businesses offer real value without locking you into one-size-fits-all policies, whether you run a food truck in Fort Lauderdale, a cleaning service in Orlando or a photography business in Sarasota. These providers rank highest:

- ERGO NEXT: Best Overall, Best for Hands-On and Service Industries

- The Hartford: Best Cheap General Liability Insurance

- biBerk: Best for Service and Activity Businesses

- Simply Business: Best for Comparing Multiple Carriers

- Coverdash: Strong for Comprehensive Coverage Needs

The profiles below cover how each insurer performs across price, claims and coverage for Florida's varied industry exposures, including the hurricane season liability risks specific to the state.