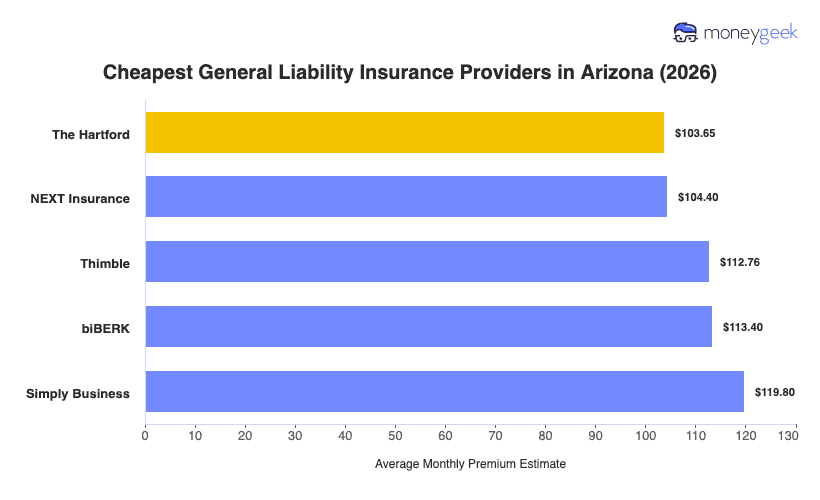

We analyzed rates across Arizona and identified four insurers with offering the cheapest general liability insurance for small businesses:

- The Hartford: Offers the lowest rates for health care providers and professional service businesses (medical practices, creative professionals, financial services)

- ERGO NEXT: Ranks cheapest across trades and customer-facing operations (construction contractors, beauty and wellness, restaurants, retail shops)

- Thimble: Often provides the most affordable coverage for specialty construction and outdoor service businesses (arborists, excavation, pest control, lawn care, remodeling)

- biBerk: Cheapest for recreation and wellness businesses (fitness centers, sports facilities, cleaning services)

[Click Each Provider to Learn More]

The most affordable commercial general liability insurance provider for your Arizona business depends on your location, business type, revenue and claims history. Use these providers as your starting point, not your final decision.