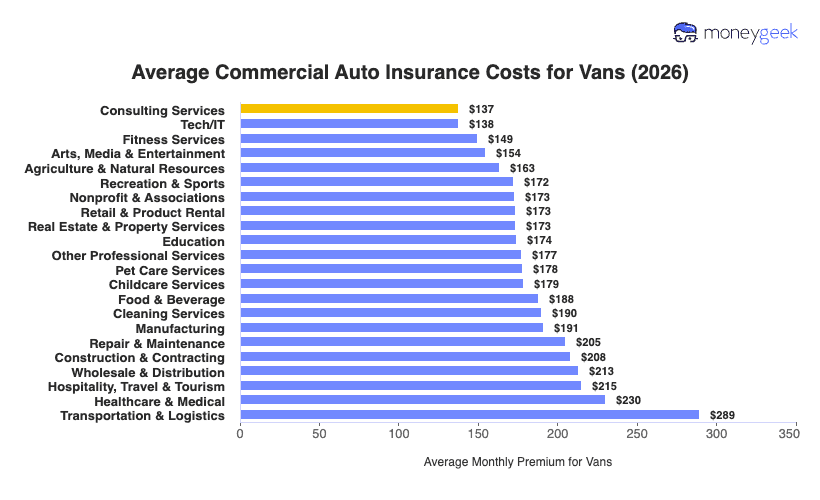

The average commercial auto insurance cost for vans is $189 per month ($2,272 a year) for minimum coverage, based on my analysis of 22 general industry areas and all states (including D.C.). It's $26 per month higher than the overall national benchmark for commercial auto policies. The higher rates are caused by the broader range of work that vans can take on, the cargo they can carry and the number of passengers they can accommodate.

However, the rates in my report should be treated as a general benchmark, and they do not represent quotes tailored to your business and vehicle profile. Your actual rates will vary widely depending on what you do with your vehicles, where you operate and how many you have within your fleet.