My commercial van insurance rankings are based on three things: what businesses actually pay for coverage, what happens when they need support and whether the policy holds up when a claim is filed. I rated providers across affordability (50%), customer experience (30%) and coverage options (20%) because price is where most businesses start the search, but it's rarely where the decision should end. For a full breakdown, see our methodology.

Best Commercial Insurance for Vans

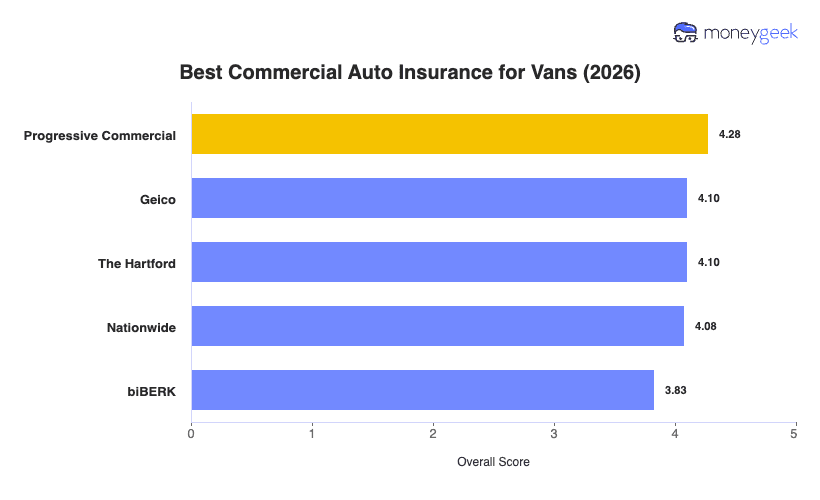

Progressive Commercial, GEICO and The Hartford are the best commercial auto insurance providers for vans, based on my analysis of affordability, customer experience and coverage depth.

Progressive Commercial ranks first overall for van commercial auto insurance, but the right fit for you depends on your industry, location and what your business actually needs from a policy.

Get matched to the best commercial auto insurer for your van and get quotes in minutes using MoneyGeek's tool below.

Select state

Updated: June 20, 2026

Advertising & Editorial Disclosure

How I Built These Best Small Business Insurer Rankings

Top Picks: Best Commercial Auto Insurance Companies for Vans

My analysis of the data shows that no single insurer stands out as the “right” commercial auto insurance provider for every van. Progressive Commercial has the highest overall score, but the best commercial auto insurance provider for you depends on three things: how your van is used, what a serious accident or cargo claim would actually cost and how much claims support your business needs when something goes wrong. Those factors play out differently for every operation, which is why the right answer for a solo florist running one cargo van looks nothing like the right answer for a healthcare company managing a fleet of passenger vans.

I picked each provider below for a specific reason, and that reason matters more than the overall ranking when your business has a particular risk profile or set of priorities:

- Progressive Commercial: Best Overall, Best for Fleet Operations

- GEICO: Best for Low-Risk Business Areas

- Nationwide: Best for Agricultural and Specialty Fleets

- The Hartford: Best for Coverage Depth

- biBerk: Best for Simple Coverage Needs

The table below shows how they ranked in this analysis for a side-by-side view.

| Progressive Commercial | 4.28 | 1 | 1 | 4 |

| Geico | 4.10 | 3 | 2 | 3 |

| The Hartford | 4.10 | 4 | 2 | 1 |

| Nationwide | 4.08 | 2 | 5 | 2 |

| biBERK | 3.83 | 5 | 4 | 5 |

I created summaries below to help you identify whether the provider is a good fit or if you need to look elsewhere. Overall rankings mean nothing if a provider doesn't match your specific operation type, industry or coverage need.

Progressive

Best Overall, Best for Fleet Operations

Progressive Commercial provides the best rates while having top marks on customer service, making it my pick as the overall best commercial auto insurance for vans. It's the largest commercial auto insurer in the U.S. by written premium and has held that position for over a decade, backed by a fully digital purchase experience, same-day coverage and a fleet telematics platform. Averaging $159 per month, it's 16% below the market average across 20 of 22 industry categories. The rate advantage thins out in agriculture, consulting and tech, where Progressive prices above the market average, and its coverage options rank fourth of five, so businesses that need deep policy customization will want to look at The Hartford.

Learn More: Progressive Business Insurance Review

GEICO

Best for Low-Risk Business Areas

GEICO is my pick for small business owners who want to get their vans covered quickly, manage everything digitally and never have to call an agent. Its entire experience is built around self-service: full online quoting, same-day coverage, instant certificates of insurance and an app that handles policy changes, driver updates and claims filing from a phone. It averages $193 per month, 2% above the market average overall, but prices 6% to 16% below average in cleaning services, hospitality, education, transportation and other professional services. It's less competitive in real estate, childcare and healthcare, where rates run 21% to 31% above average and Progressive Commercial is the better option.

Nationwide

Best for Agricultural and Specialty Fleets

Nationwide is my pick for van operations in agriculture, contracting and specialty fleet work where its combination of competitive pricing and strong coverage structure gives it a real edge. Founded in 1926 as Farm Bureau Mutual, it still has a dedicated agribusiness division with commercial auto programs built specifically for farm and agricultural operations. It averages $164 per month for van coverage, 13% below the market average, and ranks first in affordability for agriculture, consulting, recreation and other professional services. Its coverage ranks second, making it the strongest option on policy structure outside of The Hartford. The trade-off is customer experience, where it ranks last of the five providers, and its purchase process requires an agent to finalize rather than completing entirely online. Tech and fitness businesses also see rates run well above average, where Progressive Commercial or GEICO are better fits.

Learn More: Nationwide Commercial Auto Insurance Review

The Hartford

Best for Coverage Depth

The Hartford is my pick for van operations that need the strongest policy structure available, even at a higher price. It ranks first in coverage options and second in customer experience, and it's the only carrier in our analysis with a dedicated risk engineering team built into its fleet management program. With over 200 years in commercial insurance, The Hartford brings claims specialists, a self-service COI portall and written repair guarantees through its preferred network. At $220 per month on average, it runs 16% above the market average and ranks fourth on affordability, so businesses where price is the primary driver will get better value from Progressive Commercial. It's worth noting that The Hartford ranks first overall in agriculture and consulting van coverage, where its coverage structure outweighs the rate premium for the right operation.

Learn More: The Hartford Business Insurance Review

biBerk

Best for Simple Coverage Needs

biBerk is my pick for fitness, tech and IT businesses who need basic commercial coverage fast and want no broker involvement. Founded in 2015 as a Berkshire Hathaway direct-to-business brand, it's built entirely around speed. A full commercial van policy can be quoted, purchased and issued with a certificate of insurance in under 10 minutes, with 24/7 self-service for adding vehicles, updating drivers and managing billing. However, biBerk averages $212 per month, 12% above the market average overall, and ranks last on both affordability and coverage. It prices well in fitness (26% below average) and tech and IT (22% below average), but runs 20% to 37% above average in healthcare, construction, repair and maintenance, hospitality and wholesale distribution. It's also only available in 21 states.

Learn More: biBerk Business Insurance Review

Best Commercial Auto Insurance for Vans by Industry

I rank Progressive Commercial first overall in 20 of 22 industries I've analyzed, but that ranking reflects a combination of affordability, customer experience and coverage scores. In tech, recreation and professional services, Progressive actually runs above the market average, but its strong customer service still makes it the best option in those industries. In agriculture and consulting, The Hartford ranks first overall. The table below shows my picks for the best commercial van auto insurer by industry, their average monthly rate and the top provider's rate for that industry.

| Agriculture & Natural Resources | The Hartford | 2 | 2 | 1 |

| Arts, Media & Entertainment | Progressive Commercial | 4 | 1 | 4 |

| Childcare Services | Progressive Commercial | 1 | 1 | 4 |

| Cleaning Services | Progressive Commercial | 1 | 1 | 4 |

| Construction & Contracting | Progressive Commercial | 1 | 1 | 4 |

| Consulting Services | The Hartford | 4 | 2 | 1 |

| Education | Progressive Commercial | 1 | 1 | 4 |

| Fitness Services | Progressive Commercial | 3 | 1 | 4 |

| Food & Beverage | Progressive Commercial | 1 | 1 | 4 |

| Healthcare & Medical | Progressive Commercial | 1 | 1 | 4 |

| Hospitality, Travel & Tourism | Progressive Commercial | 1 | 1 | 4 |

| Manufacturing | Progressive Commercial | 1 | 1 | 4 |

| Nonprofit & Associations | Progressive Commercial | 1 | 1 | 4 |

| Other Professional Services | Progressive Commercial | 3 | 1 | 4 |

| Pet Care Services | Progressive Commercial | 1 | 1 | 4 |

| Real Estate & Property Services | Progressive Commercial | 1 | 1 | 4 |

| Recreation & Sports | Progressive Commercial | 3 | 1 | 4 |

| Repair & Maintenance | Progressive Commercial | 1 | 1 | 4 |

| Retail & Product Rental | Progressive Commercial | 1 | 1 | 4 |

| Tech/IT | Progressive Commercial | 3 | 1 | 4 |

| Transportation & Logistics | Progressive Commercial | 1 | 1 | 4 |

| Wholesale & Distribution | Progressive Commercial | 1 | 1 | 4 |

The best commercial auto insurance for vans depends heavily on what your business does. These pages break it down by industry:

What Determines the Best Commercial Auto Insurance for Vans for You

The best commercial auto insurance for vans isn't defined by a single factor. The right provider balances affordability across your industry, offers coverage that matches how your van is actually used and features a claims process you can count on when you need it. Three areas matter most when evaluating which insurer fits your business.

- Liability limits: State minimums are a starting point, but your actual needs will depend on your risk profile. For passenger vans, a single serious accident with multiple occupants generates a separate bodily injury claim from each person in the vehicle simultaneously, and a policy at minimum limits can be exhausted before the first claimant is fully paid out.

- Vehicle use classification: How the van is used and what it carries affects both eligibility and pricing. Confirm the carrier covers your specific use, whether that's service calls, deliveries, passenger transport or cargo hauling, before buying.

- Cargo and equipment protection: Tools, goods and specialized equipment inside the van are not covered by commercial auto insurance. If your operation depends on what's in the van, inland marine or motor truck cargo coverage needs to be part of the conversation.

- Hired and non-owned auto: If employees ever use personal vehicles or rented vans for business purposes, this coverage extends your liability to those vehicles. It's one of the most commonly skipped endorsements and one of the most frequently needed.

- Deductible structure for fleets: Most van policies apply a deductible per vehicle per incident. If multiple vans are involved in the same accident, you pay the deductible multiple times. Ask whether the carrier offers a fleet deductible structure, and confirm that newly added vans are covered automatically for 30 days after purchase. Most carriers include that window, but you have to notify them to extend coverage beyond it.

- Passenger liability: Vans used for shuttle services, non-emergency medical transport or any passenger-carrying use have per-passenger bodily injury exposure. Each person in the van at the time of a serious accident is a potential claim, which changes how much liability coverage your operation actually needs.

Affordability Across Your Industry and Use Case

Van commercial auto pricing swings significantly by industry category, and the gap between the most and least expensive carrier for the same type of business can be substantial. In wholesale and distribution, rates range from $146 to $293 per month across the five providers in this analysis. Transportation and logistics, repair and maintenance and healthcare operations show similar gaps of $100 or more per month between the most and least competitive carriers. That's why I recommend that you get quotes from multiple providers before making a decision, especially if your industry is among the aforementioned.

Coverage That Matches Your Fleet's Risks

Your commercial van insurance needs to match what the insured van actually does and carries. A cargo van hauling equipment for a contractor has different coverage needs than a passenger van transporting clients, and a fleet of healthcare vans running daily routes has different risk exposure than a single vehicle used for occasional deliveries. Pay close attention to these when evaluating policies:

Customer Experience and Claims Support

Commercial van claims work differently from personal auto coverage, and the service quality gap between carriers shows up most clearly when a vehicle is out of commission and the business is waiting on a repair or a settlement. Check whether the claims team is available around the clock or only during business hours, whether your claim gets a dedicated commercial adjuster or goes through a general call center, and whether you'll have a consistent point of contact throughout the process. NAIC complaint ratios give you an unbiased benchmark, but it's also a good idea to check provider reviews from forums on Reddit and Facebook.

How to Choose the Best Commercial Auto Insurance for Vans

Most van operators who overpay for coverage don't pick the wrong carrier. They describe their operation incorrectly at the quote stage and get placed in the wrong risk category. These steps get you to the right policy at the right price.

- 1Define Your Risk Profile

Catalog every van in operation as owned, leased or employee-owned but used for business. Document the primary use of each van, annual mileage per vehicle and the driving records of everyone behind the wheel. Mileage matters because carriers tier rates by annual miles driven, and the difference between 10,000 and 25,000 miles per year on the same van can move you into a higher pricing bracket with some underwriters. If you're in healthcare, construction, transportation and cleaning services, carefully study your use classification, since how the van is used and what it carries directly affects both pricing and which carriers will write the policy.

- 2Determine Your Coverage Requirements

With your risk profile documented, identify which coverage types your operations actually require beyond the state minimum. For van operations, that typically means:

- Vans transporting goods or cargo for others need motor truck cargo coverage. This applies to healthcare supply delivery, wholesale distribution and any operation where freight in transit is the business.

- Financed or leased vans require collision and comprehensive coverage. Without it, a total loss leaves you owing the lender more than the insurance check covers.

- Operations where employees use personal or rented vans for business need hired and non-owned auto coverage. Without it, an employee's personal auto policy is the only line of defense when they're running a work errand in their own vehicle, and personal policies routinely exclude business use.

- Passenger vans used for for-hire transport, shuttle services or non-emergency medical transport may trigger higher state minimum liability requirements and, for interstate operations, FMCSA minimums of $1.5 million for 6 to 15 passengers. A cleaning company shuttling its own employees doesn't hit that threshold, but a shuttle service charging fares does.

- Service vans carrying tools or equipment need inland marine coverage for the contents. Commercial auto covers the vehicle, not what's inside it.

- 3Research Providers by Industry and Vehicle Type

Not all carriers price van risk the same way, and the classification conversation happens before the quote. Call shortlisted carriers and ask directly how they classify your specific van use: service, delivery, passenger transport or cargo hauling. The same operation gets classified differently by different underwriters, and that classification drives the premium more than any other single factor. Identify which carriers have demonstrated pricing strength in your industry using the industry data earlier on this page, then confirm their classification treatment before investing time in a full quote.

- 4Evaluate Coverage Quality and Policy Terms

Comparing premiums tells you what a policy costs, but comparing policy terms tells you what you're actually buying. For each shortlisted provider, check which coverages are standard versus endorsement-only, what liability limits are available and what exclusions could affect a claim. Confirm how the policy handles mid-term additions. Most carriers include a 30-day automatic coverage window when you add a van, but you have to notify them before that window closes or the new vehicle isn't covered.

- 5Get Quotes to Confirm

Request quotes only after narrowing your options through research. A quote validates whether a provider's pricing holds for your specific fleet, location and coverage requirements. If a quote comes back higher than expected, check the vehicle use classification you inputed before ruling out the carrier. Listing a delivery van as a service vehicle is one of the most common reasons quotes reprice significantly at underwriting, and correcting it early saves time on both sides.

- 6Confirm Filing Requirements Before the Policy Binds

If you're not sure whether your operation triggers federal filing requirements, ask the carrier whether your specific van use requires additional filings before the policy binds. Most standard van operations don't cross the threshold, but two situations consistently do:

- Vans used in interstate commerce with a gross vehicle weight rating over 10,001 pounds require a U.S. Department of Transportation number and a federal insurance endorsement that makes the policy a direct obligation to injured members of the public.

- Vans carrying passengers for compensation may require state-level for-hire operating authority depending on the state and passenger count.

A carrier that knows your operation upfront can confirm whether filings apply and build them into the policy correctly from day one.

Best Commercial Auto Insurance for Vans: Bottom Line

When choosing the best commercial auto insurance for your van, ask yourself: what does your van actually do for the business, what industry are you operating in and what would a serious accident actually cost? Your answers narrow the field faster than any rate comparison, because pricing and coverage fit vary more by use case and industry. I recommend that you carefully study these factors before you look at a single premium.

Not every provider fits every business, and the lowest-premium policy isn't always the best value if it leaves gaps in coverage. Think about whether you want a fully digital, self-service experience where you handle everything online or agent-supported guidance with someone who knows your account. From there, two or three quotes confirm whether the right fit on paper holds up for your specific fleet and requirements.

Best Commercial Van Insurance: Next Steps

For most van operations, the right starting point is getting quotes from Progressive Commercial and GEICO. Progressive Commercial is the strongest overall option, leadig on affordability and customer experience across the widest range of industries and use cases. GEICO is the better fit for smaller, service-oriented operations that want a fully digital, self-service experience without an agent. If your van operation involves agriculture, consulting, or complex coverage needs, I recommend adding The Hartford to your list.

Recommended: If You're Ready to Get Quotes Now

By this point you should know your fleet composition, your coverage requirements and which providers match your industry and van use case. Request quotes from at least three providers and compare both price and policy terms before committing. If a quote comes back higher than expected, check your coverage selections and vehicle use classification before ruling out a provider.

If You Want to Confirm Cost Before Deciding

Pricing for commercial van insurance varies a lot by industry and use case. A wholesale distribution van and a consulting firm's cargo van can price out very differently with the same carrier. Use the resources below to ground your cost expectations before reaching out to any provider.

If You're Unsure What Coverage Your Fleet Needs

Start by mapping your actual exposure: what vans you operate, how they're used, what they carry and whether employees use personal vehicles for business. Each factor points to a specific coverage type, and missing one creates a real gap in financial protection.

If You Have Specialized Filing Requirements

Passenger-carrying vans used for for-hire transport, shuttle services or non-emergency medical transport may require state-level operating authority and higher minimum liability limits before a standard commercial auto policy is sufficient. Vans operating in interstate commerce with a gross vehicle weight rating over 10,001 pounds trigger federal filing requirements including a U.S. Department of Transportation number and a federal insurance endorsement. Confirm with your carrier whether your operation falls into either category before the policy binds.

How We Chose the Best Commercial Van Insurance Companies

Our goal was to identify which providers deliver the most consistent overall value across the three dimensions that matter most to business owners: what they pay, how well they're covered and how the carrier performs when they need support. Five providers made the cut for our van analysis: Progressive Commercial, GEICO, The Hartford, Nationwide and biBerk. We analyzed all five across 22 general industry categories covering transportation, healthcare, construction, cleaning services, food and beverage, agriculture and 17 other specific industry areas.

Our Scoring Model

We scored each of the five providers across three weighted categories that combine into an overall score out of 5.

- Affordability (50% of overall score): We measured how competitively and consistently each provider prices van commercial auto coverage across industries and states, benchmarked against average rates.

- Customer Experience (30% of overall score): We evaluated how well each provider supports businesses across the full policy lifecycle, buying, policy management and claims handling.

- Coverage Options (20% of overall score): We assessed how well each provider addresses common van fleet risks and how much flexibility it allows across coverage types and endorsements.

Learn more about our methodology.

About Mark Flores

Mark Flores is a Business Insurance Content Writer at MoneyGeek. He covers commercial auto, commercial property, cyber and specialty insurance so business owners can understand what a policy covers, what it excludes and how to choose a provider beyond the standard pitch.

Before MoneyGeek, Mark spent over a year at Clutch.co as a Senior Content Writer. He produced structured B2B reviews and provider analyses from client interviews and service evaluations. The approach mirrors how commercial insurance teams build content: research companies, analyze performance data and turn findings into objective comparisons. Mark has also spent nearly four years as a digital marketing specialist for small business clients in home services, manufacturing and education. That work put him inside the operational decisions behind commercial insurance.

At MoneyGeek, he put in nearly five years in the credit cards vertical before moving to business insurance. That research and editorial grounding runs through his coverage guides, provider comparisons and cost analyses.

Linkedin: https://www.linkedin.com/in/mark-jason-flores-7844634a/

Contact Email: mark.flores@moneygeek.com