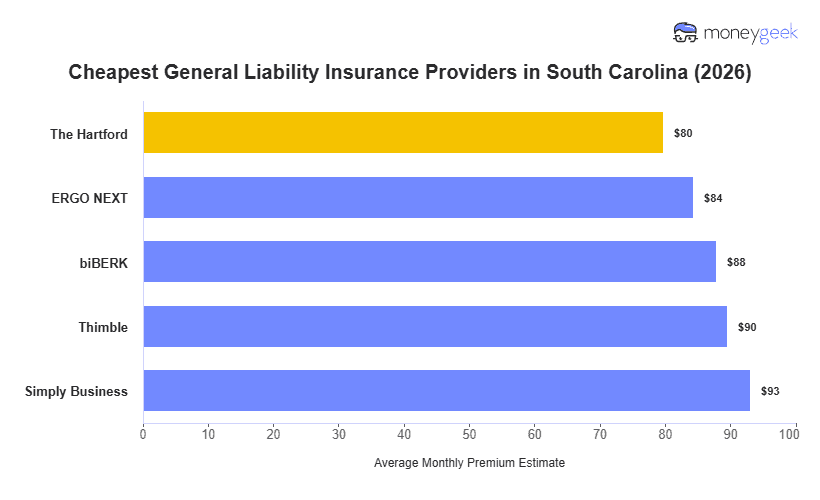

The cheapest general liability insurance in South Carolina depends on what kind of work you do, since insurers price a Hilton Head catering company differently than a Greenville contractor or a Columbia accounting firm. Our analysis of over 400 business types in the state showed these providers offer the lowest rates:

- The Hartford: Most affordable for professional services and health care providers (bookkeeping services, financial advisors, dental practices, chiropractic offices)

- ERGO NEXT: Lowest rates for construction contractors and personal services (electrical contractors, plumbing contractors, barber shops, nail salons)

- biBerk: Cheapest for cleaning services and fitness businesses (janitorial services, carpet cleaning, gyms, yoga studios)

- Simply Business: Most affordable for brick-and-mortar retail and food service (clothing stores, bookstores, full-service restaurants, bakeries)

[Click Each Provider to Learn More]

Your actual premium reflects how insurers assess your particular operation: a Lowcountry tour guide faces different liability exposures than a Florence manufacturing shop. Start with the insurer that usually prices your industry type lowest, then compare quotes to find your best rate.