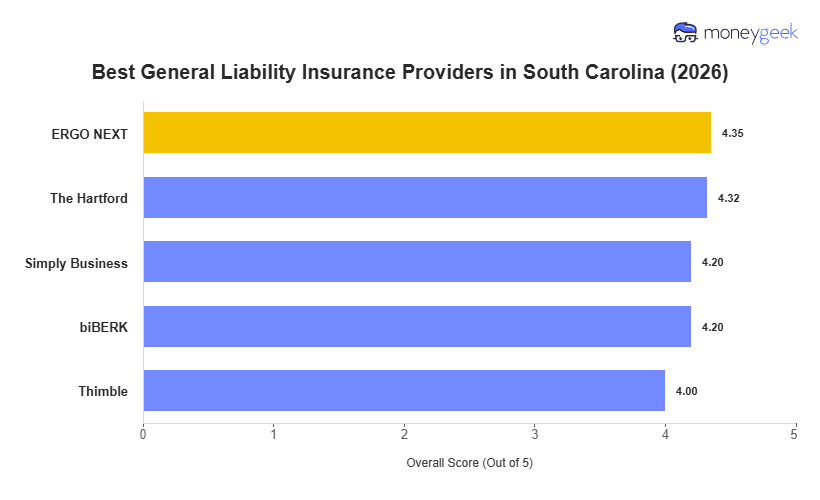

The best general liability insurance companies for South Carolina small businesses deliver reliable coverage without overcharging. We analyzed 10 major providers across 408 business types for policies with $1 million per occurrence and $2 million aggregate limits and found these insurers topped our list:

- ERGO NEXT: Best Overall, Best for Hands-On Industries

- The Hartford: Best Cheap General Liability Insurance

- Simply Business: Best for Consumer-Facing Service Businesses

- biBerk: Best for Sole Proprietors

- Thimble: Best for On-Demand and Short-Term Coverage

These providers hold up well on pricing, service quality and coverage breadth for South Carolina operations. The profiles below break down where each insurer pulls ahead, whether you run a Myrtle Beach retail shop, a Columbia professional services firm or a Greenville contractor business.