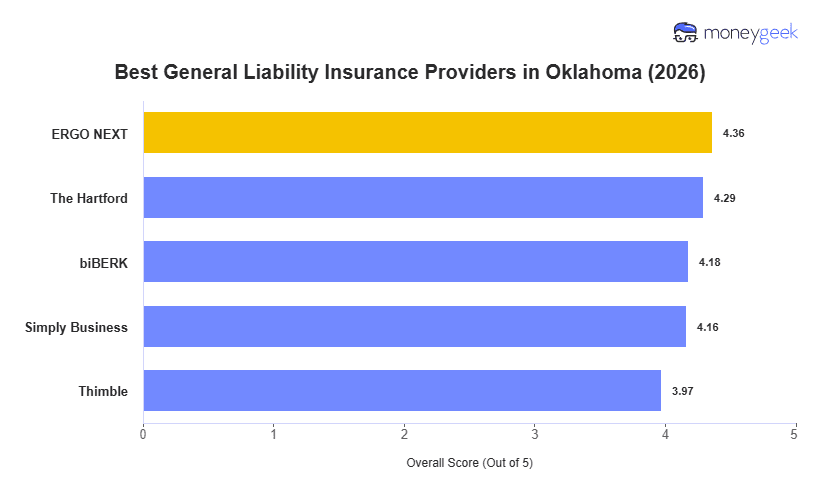

MoneyGeek analyzed 10 major general liability insurers across 25 industries to identify the best and most affordable options for Oklahoma small businesses. The right provider varies by business, but these five ranked high for pricing, service quality and coverage options in Oklahoma.

- ERGO NEXT: Best Overall, Best for Hands-On Industries

- The Hartford: Best for Professional and Licensed Industries

- Simply Business: Best for Service-Based Businesses

- biBerk: Best for Comparing Carrier Options

- Thimble: Best for Freelancers and Gig Workers

The table below shows how each provider ranks and what Oklahoma businesses can expect to pay. A drilling contractor near Cushing or a boutique owner in Norman preparing for spring storm season can use this breakdown to weigh cost against coverage.