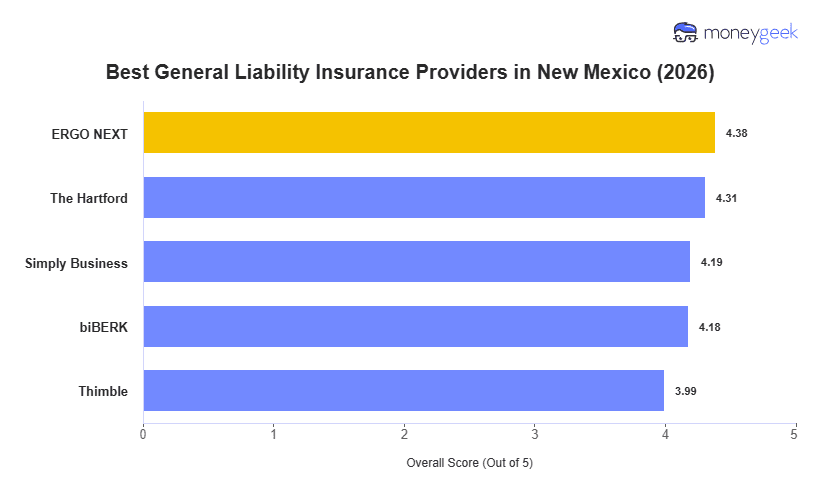

New Mexico business owners need more than a low premium to get real value from general liability coverage. MoneyGeek reviewed 10 major carriers across 408 business categories, weighing rates, coverage options and customer experience to find the best fits. Five insurers rose to the top:

- ERGO NEXT: Best Overall, Best for Hands-On and Hospitality Businesses

- The Hartford: Best Cheap General Liability Insurance

- Simply Business: Best for Simultaneously Shopping Multiple Insurers

- biBerk: Best for Fitness and Recreation Businesses

- Thimble: Best for On-Demand Coverage

General liability needs vary widely across New Mexico industries, from food service operations to outdoor recreation businesses. This table breaks down each provider's scores and estimated monthly rates: