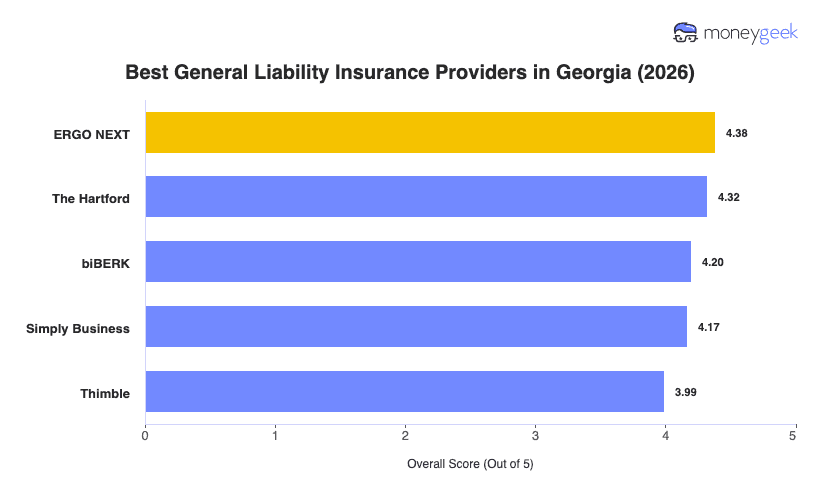

A Marietta landscaping crew and a Buckhead consulting practice have almost nothing in common, but both need general liability coverage that fits their actual risk without overpaying. Our analysis of Georgia small businesses identified these five best general liability insurance providers:

- ERGO NEXT: Best Overall, Best for Hands-On and Service Industries

- The Hartford: Best for Professional Services

- biBerk: Best for Service Businesses

- Simply Business: Best for Comparing Carriers

- Thimble: Best for On-Demand Coverage

Each insurer on this list performs well across affordability, customer experience and coverage strength. The breakdowns below explain how each earned its ranking and where it fits for Georgia small business owners.