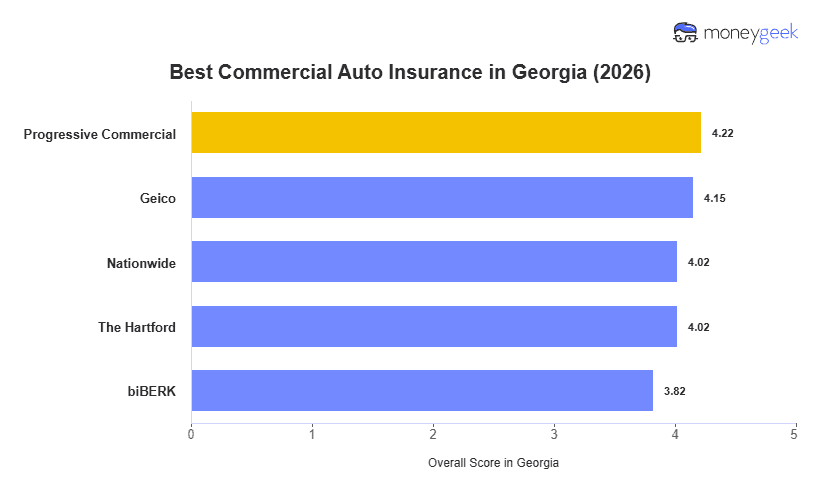

No single insurer is the right best commercial auto insurance option for every Georgia business, and the data bears that out. Progressive ranks first overall, but the right carrier depends on three things specific to the operation: what vehicles the business operates, what a serious claim would cost the business and how much support it needs when something goes wrong. A landscaping contractor running a single pickup truck in rural Georgia will reach a very different conclusion than a logistics company managing a mixed fleet out of Atlanta.

Each provider below earned its spot for a specific reason, and that reason matters more than the overall ranking when a business has a particular vehicle profile, risk level or set of priorities:

- Progressive: Best Overall, Best for Fleet Operations

- GEICO: Best for Low-Risk Business Areas

- Nationwide: Best for Agricultural and Specialty Fleets

- The Hartford: Best for Coverage Depth

- biBerk: Best for Simple Coverage Needs

The table below shows how these providers ranked across affordability, customer experience and coverage in this Georgia analysis for a side-by-side view to ground the comparison.