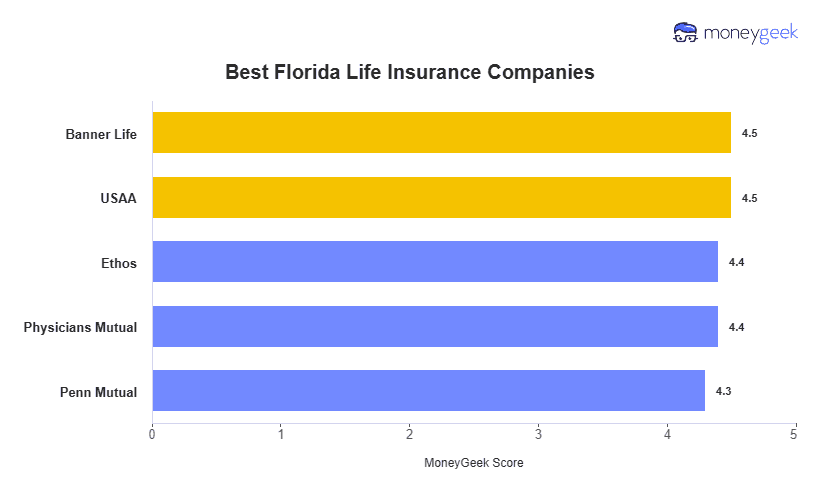

The best life insurance in Florida depends less on which carrier you pick and more on which policy type fits your situation. A 40-year-old nonsmoking woman buying a 20-year term policy pays $37 per month with Banner Life for $500,000 in coverage. The same person buying whole life through USAA pays $504 per month for the same death benefit. That $467 monthly gap buys a policy that never expires and builds cash value you can borrow against, versus one that covers you for exactly 20 years and has no cash value growth. If you're buying life insurance primarily to cover a mortgage or income replacement for a fixed period, term is almost always the better value. If you're building long-term wealth or need coverage that doesn't expire, the permanent options below are worth the higher cost.

For buyers who want to skip the medical exam, Ethos provides fully online IUL applications with approvals in minutes, while Penn Mutual offers up to $10 million in no-exam coverage and has the lowest NAIC complaint index of any provider we reviewed. Physicians Mutual has the lowest guaranteed acceptance rates in our analysis, at $52 per month for a 55-year-old woman.