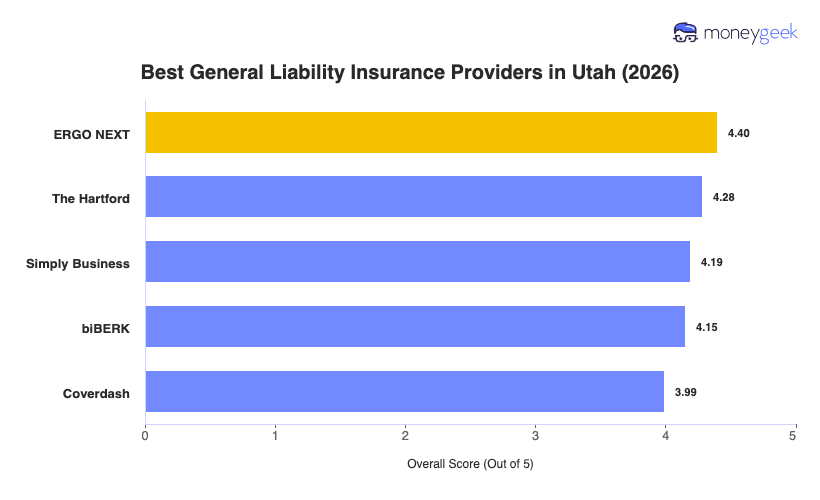

No single general liability insurer fits every Utah business, but these five providers rank highest across the state for balancing cost, service quality and coverage strength, whether you run a one-person operation or manage a growing team. MoneyGeek analyzed 10 major insurers across 25 general industries to identify the best general liability insurance companies for Utah small businesses.

- ERGO NEXT: Best Overall, Best for Digital-First Buyers

- The Hartford: Best for Professional Services

- Simply Business: Best for Carrier Choice

- biBerk: Best for Personal Services

- Thimble: Best for Flexible-Term Coverage

These five carriers cover the range of Utah business risks, from slip-and-fall claims at Provo retail shops to equipment damage allegations at Ogden construction sites. The profiles below break down pricing, coverage options and fit for Utah's industry mix.