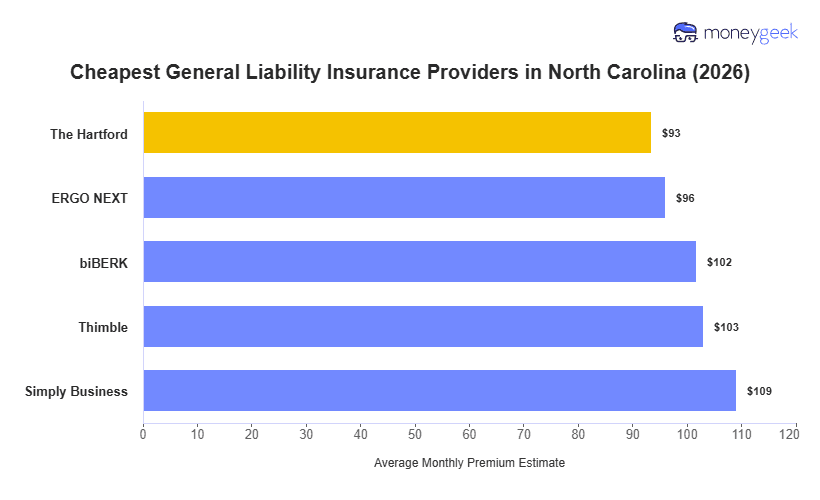

Finding the cheapest general liability insurance in North Carolina starts with knowing which providers consistently offer the lowest rates for your industry. Our analysis of 25 general showed these results:

- The Hartford: Cheapest for creative professionals and health care providers, including photography, videography, art galleries and dental practices

- ERGO NEXT: Lowest rates for construction trades and food service businesses, such as general contractors, HVAC contractors, restaurants and food trucks

- biBerk: Most affordable for cleaning services and fitness facilities, including house cleaning, janitorial services, gyms and yoga studios

- Simply Business: Cheapest for retail stores and specialty food businesses, such as clothing stores, bookstores, bakeries and daycare centers

- Thimble: Best rates for general construction and engineering services, including electricians, engineering firms and land surveyors

[Click Each Provider to Learn More]

Your final premium scales with factors like annual revenue, employee count and the physical risks your work involves. Treat these sweet spots as a starting point, not a guarantee. Compare quotes from multiple insurers to find your actual lowest rate.