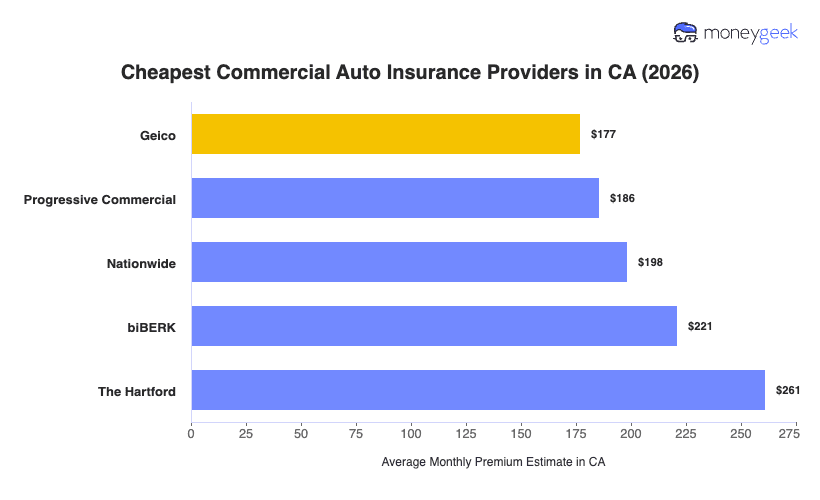

These are the cheapest commercial auto insurance providers in California, all with rates below the state average. Which one saves your business the most depends on your industry and the vehicles you operate.

- GEICO averages $177 per month for commercial auto insurance in California, 15% below the state average. It ranks first in affordability across 14 of 25 general industry categories in MoneyGeek's California analysis, with its strongest savings concentrated in financial services, education and consulting. GEICO also prices lowest for sedans, SUVs, pickup trucks and farm tractors.

- Progressive Commercial averages $186 per month, 11% below the California state average. It leads on affordability for 10 general industry categories, including transportation and logistics, wholesale and distribution, manufacturing and hospitality. Progressive Commercial prices lowest for vans, food trucks, taxis and limousines, with savings reaching 31% below the state average for taxi and limousine fleets.

- Nationwide averages $198 per month, 5% below the California state average. It doesn't lead any general industry category in MoneyGeek's California analysis but remains a competitive third option for businesses whose industry and vehicle profile don't align with GEICO or Progressive Commercial's strongest segments.

Actual California commercial auto insurance costs vary by vehicle fleet details, driver records, services offered and location within the state. Use these rankings as a starting point for comparison, not a final decision.