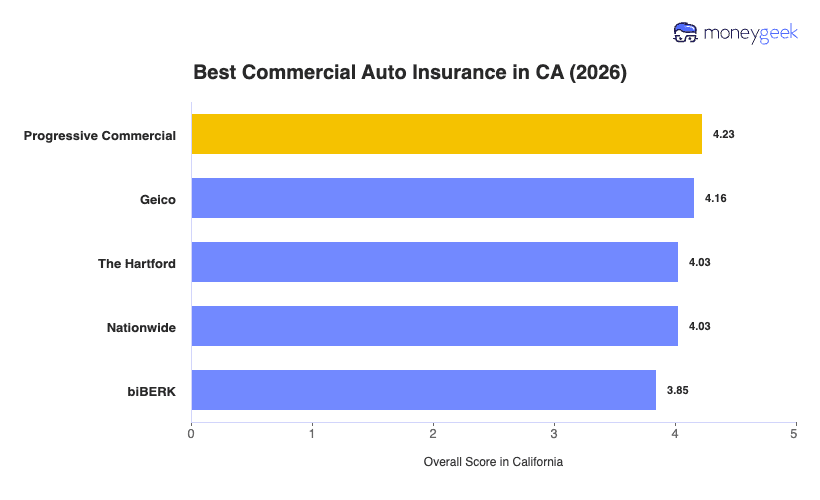

Most businesses can find the best commercial auto insurance in California with these providers:

- Progressive Commercial: Best Overall, Best for Fleet Operations

- GEICO: Best for Low-Risk Business Areas

- The Hartford: Best option for Coverage Depth

- Nationwide: Best choice for Agricultural and Specialty Fleets

- biBerk: Best for Simple Coverage Needs

California businesses range from solo contractors with one pickup truck to logistics companies running multi-vehicle fleets, and no single provider wins across every scenario. The right choice comes down to what vehicles the business operates, what industry it's in and how much coverage depth the operation actually requires.