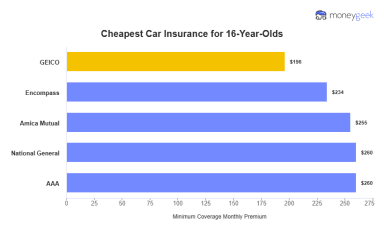

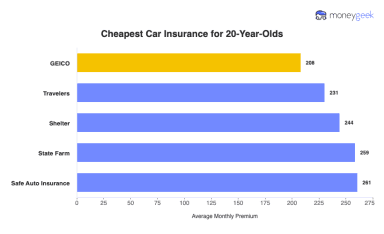

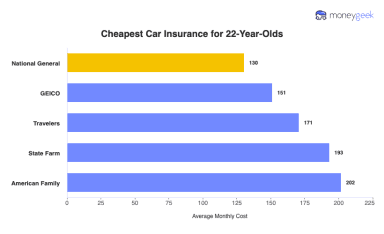

Car insurance gets cheaper as you gain driving experience and keep a clean record. For most drivers, rates drop the most between ages 16 and 24. Insurers review your risk at certain ages, and those reviews often lead to lower premiums.

Past your mid-20s, age stops being the dominant factor. What you pay from that point is mostly a product of your record, your claims history and the coverage you carry.