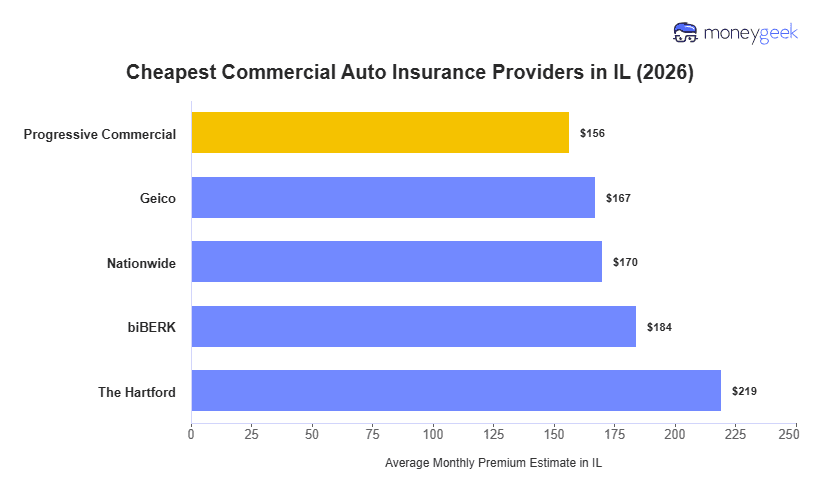

These are the cheapest commercial auto insurers in Illinois, all pricing below the state average of $179 per month.

- Progressive Commercial averages $156 per month for commercial auto insurance in Illinois, 13% below the state average. It ranks first in affordability for 16 of 25 general industries in MoneyGeek's Illinois analysis, with its strongest savings in Wholesale & Distribution (31% below average), Manufacturing and Transportation & Logistics (both 25% below average).

- GEICO averages $167 per month, 7% below the Illinois state average. It prices most competitively for office-based and service-sector businesses, ranking first for Consulting Services (18% below average), Marketing & Communications (27% below average) and Pet Care Services (8% below average). GEICO also ranks first for sedans and SUVs among all vehicle types studied.

- Nationwide averages $170 per month, 5% below the Illinois state average. It doesn't lead any specific industry or vehicle category in MoneyGeek's Illinois data, but it's the third-cheapest option overall and a reasonable fit for businesses whose industry or vehicle type isn't covered by Progressive Commercial or GEICO.

Actual Illinois commercial auto insurance costs vary by vehicle fleet details, driver records, services offered and location within the state, so these rankings won't apply to every Illinois business. Use these companies as a starting point to compare Illinois commercial auto insurance costs before committing to a policy.