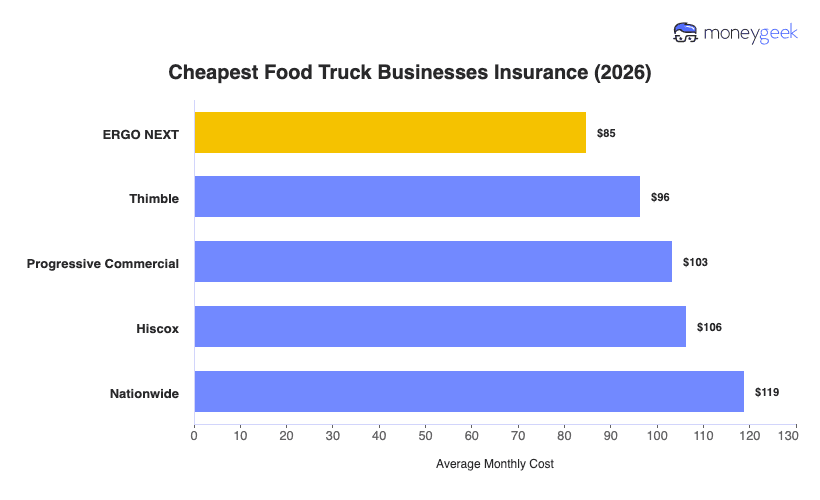

Insurers price food truck policies differently than restaurant coverage because the exposure combines a commercial kitchen with a street-operated vehicle, health permit dependencies and public-facing liability that shifts with every location. ERGO NEXT is the cheapest overall, followed by Thimble and Progressive Commercial. Only three of the seven providers we analyzed price below the food truck sub-industry average. The spread between the three is roughly $19 a month, so once you're comparing providers in this tier, coverage fit matters more than chasing the last few dollars of price difference.

The most affordable business insurance for food truck companies depends on your coverage mix, crew size and operating state. A two-person truck running daily permitted stops prices differently than a solo operator at a fixed weekly market, and those variables shift which of the three leads for your operation.