ERGO NEXT leads Massachusetts business insurance with excellent customer service, competitive rates and comprehensive coverage options. The Hartford and Simply Business provide quality coverage for Massachusetts entrepreneurs.

Best Small Business Insurance in Massachusetts

Massachusetts business owners choose ERGO NEXT, The Hartford, and Simply Business for top coverage with rates starting at $76 yearly.

Get matched to the best Massachusetts commercial insurer for you below.

Select your industry

Select state

Updated: March 17, 2026

Advertising & Editorial Disclosure

Business Insurance in Massachusetts: Key Takeaways

ERGO NEXT offers Massachusetts' best small business insurance with top customer service scores and rates ranking second for affordability.

The Hartford offers the cheapest small business insurance in Massachusetts at $88 monthly ($1,054 annually).

Choosing the right small business insurance coverage means comparing quotes, assessing risks and using discounts.

Get Matched to the Best Small Business Insurance Providers in Massachusetts

Select your industry and state to get a customized quote for your Massachusetts business.

Industry

State

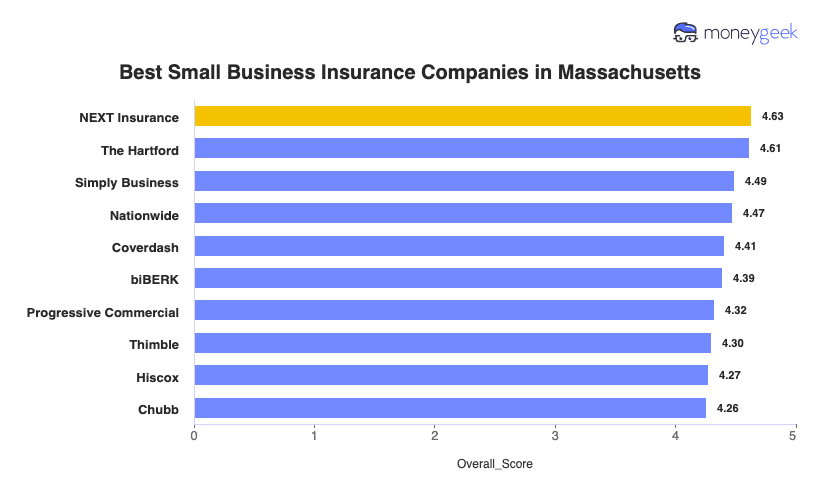

Best Small Business Insurance Companies in Massachusetts

| ERGO NEXT | 4.63 | $105 | 1 | 2 |

| The Hartford | 4.61 | $88 | 2 | 3 |

| Simply Business | 4.49 | $101 | 5 | 1 |

| Nationwide | 4.47 | $107 | 2 | 4 |

| Coverdash | 4.41 | $106 | 6 | 2 |

| biBERK | 4.39 | $109 | 2 | 5 |

| Progressive Commercial | 4.32 | $104 | 7 | 5 |

| Thimble | 4.30 | $99 | 8 | 5 |

| Hiscox | 4.27 | $113 | 4 | 6 |

| Chubb | 4.26 | $124 | 3 | 4 |

Note: These rates reflect MoneyGeek's analysis of small businesses with two employees across 79 major industries. Your actual rates vary based on your industry risk factors, claims history, coverage limits and individual insurer underwriting criteria. Contact insurers directly for personalized quotes.

RESEARCH THE BEST BUSINESS INSURANCE IN MASSACHUSETTS BY COVERAGE TYPE

Discover the best or cheapest business insurer in Massachusetts for your desired coverage type in our resources below:

ERGO NEXT

Best Massachusetts Business Insurance

MoneyGeek Rating

4.6/ 5

4.5/5Affordability

4.7/5Customer Experience

4.8/5Coverage Options

Average Monthly Cost of General Liability Insurance

$108This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$72This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Survey: Digital Experience

4.8/5 (1st)Our Survey: Likely to Be Recommended to Others

4.8/5 (1st)

The Hartford

Cheapest Massachusetts Business Insurance

MoneyGeek Rating

4.6/ 5

4.6/5Affordability

4.6/5Customer Experience

4.7/5Coverage Options

Average Monthly Cost of General Liability Insurance

$86This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$73This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Survey: Claims Process

4.5/5 (1st)Our Survey: Agent Service

4.7/5 (1st)

Simply Business

Best Commercial Coverage Options in Massachusetts

MoneyGeek Rating

4.5/ 5

4.4/5Affordability

4.2/5Customer Experience

4.9/5Coverage Options

Average Monthly Cost of General Liability Insurance

$100This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$75This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Research: Digital Experience

4.5/5Our Survey: Service Quality

4.0/5

How to Get the Best Cheap Small Business Insurance in Massachusetts

Massachusetts small business owners face winter storms closing offices statewide, workers' compensation requirements from the first hire and new commercial auto minimums. Getting business insurance means preparing for these legal requirements and seasonal disruptions.

- 1

Know what Massachusetts law requires versus what protects your business

Massachusetts law requires workers' compensation from your first employee—even part-time hires, with a 16-hour weekly minimum only for domestic workers. Commercial vehicles need 25/50/30 coverage starting July 2025, the first increase in four decades. Liquor liability isn't state-mandated, but Cape Cod restaurants serving alcohol need it when intoxicated customers cause accidents, and landlords require proof before leasing bar space.

- 2

Address hazards unique to your Massachusetts operation

February 2024 winter storms brought eight to 12 inches of snow statewide, closing government offices and causing scattered power outages. Cambridge biotech labs without business interruption coverage absorbed lost revenue while refrigeration systems failed and research samples spoiled. Worcester manufacturers need commercial property insurance covering costs from power outages damaging CNC machines and inventory during severe weather.

- 3

Compare standard carriers with Massachusetts specialty programs

ERGO NEXT, The Hartford and Simply Business offer competitive Massachusetts rates, but if two carriers reject your Route 128 startup or Worcester machine shop because of high-risk operations or past claims, Massachusetts's assigned risk pool offers workers' compensation through the Workers' Compensation Rating and Inspection Bureau. Assigned risk premiums exceed standard market rates, so exhaust traditional carriers first.

- 4

Don't sacrifice claims service for the lowest premium

February 2024 winter storms closed government offices and created hazardous travel across Massachusetts, separating responsive insurers from slow ones. Boston financial consultants losing client billings or Cape Cod restaurants losing tourism revenue can't wait three weeks for business interruption checks. Ask carriers about Massachusetts adjuster counts and average claim resolution times before committing to the cheapest option.

- 5

Stack discounts and pay annually to cut costs

Bundle general liability with commercial property in a business owner's policy to reduce combined premiums and pay annually instead of monthly to avoid installment fees. Massachusetts insurers reward claim-free years and safety training completion. Cambridge biotech labs completing lab safety certifications or restaurants completing food handler training stack these discounts with bundling, reducing total insurance spend.

- 6

Reassess your policies after Massachusetts growth milestones

Massachusetts's one-employee workers' compensation threshold triggers mandatory coverage when you hire. Expanding from Baltimore to the Eastern Shore means different premium rates, since Montgomery County businesses pay 18% to 32% more than rural areas. Landing contracts with federal agencies often requires $2 million aggregate limits. Review your business insurance costs before growth happens, not after you're already committed and exposed.

Best Business Liability Insurance Massachusetts: Bottom Line

ERGO NEXT leads Massachusetts for customer service while The Hartford offers the state's lowest rates at $88 monthly. Compare quotes from both, assess your business risks and stack available discounts to find coverage that protects your operation without overpaying.

Business Insurance Massachusetts: FAQ

Small business owners in Massachusetts often have questions about choosing the right business insurance. We answer the most common concerns below:

What insurance do I need for my small business in Massachusetts?

Massachusetts requires workers' compensation from your first hire and commercial auto at 25/50/30 minimums starting July 2025. General liability isn't state-mandated, but landlords and clients require proof before contracts. Cambridge biotech labs need equipment coverage, while Cape Cod restaurants serving alcohol should add liquor liability.

How much does small business insurance cost in Massachusetts?

Coverage costs for your Massachusetts business depend on employee count, claims history and industry risk level, but these are the monthly and annual averages by coverage type:

- General liability insurance: $109 monthly or $1,303 annually

- Workers' compensation insurance: $77 monthly or $925 annually

- Professional liability (E&O) insurance: $82 monthly or $980 annually

- Business owner's policy (BOP): $155 monthly or $1,858 annually

Do I need general liability, or should I get a Business Owner's Policy (BOP)?

Start with general liability if you're a solo consultant because it covers customer injuries at $109 monthly. BOPs bundle general liability with commercial property for $155 monthly, saving 20% to 30% for Worcester manufacturers and Boston storefronts. Get a BOP if you own equipment, inventory or lease space.

Do I need workers' comp in Massachusetts if I hire my first employee?

Yes, Massachusetts requires workers' compensation from your first employee, stricter than neighboring states. The only exception is domestic workers under 16 hours weekly. Coverage costs $77 monthly and protects you from $100 daily fines and Stop Work Orders. Get quotes from ERGO NEXT or The Hartford before your hire date.

How do I get proof of insurance (a COI) for a landlord or client in Massachusetts?

Request a certificate of insurance from your insurer online, by phone or through your agent—most issue COIs within 24 hours at no charge. The certificate lists coverage limits and names your landlord or client as "additional insured." Cambridge tech startups need COIs before signing leases or landing Mass General contracts.

About Mark Fitzpatrick

Mark Fitzpatrick, a Licensed Property and Casualty Insurance Producer, is MoneyGeek's resident Personal Finance Expert. He has analyzed the insurance market for over five years, conducting original research for insurance shoppers. His insights have been featured in CNBC, NBC News and Mashable.

Fitzpatrick holds a master’s degree in economics and international relations from Johns Hopkins University and a bachelor’s degree from Boston College. He's also a five-time Jeopardy champion!

He writes about economics and insurance, breaking down complex topics so people know what they're buying.

sources

- Commonwealth of Massachusetts. "Healey-Driscoll Administration Issues Safety Reminders Ahead of Anticipated Winter Storm." Accessed March 24, 2026.

- Commonwealth of Massachusetts. "New Motor Vehicle Mandatory Coverage Limits." Accessed March 24, 2026.

- Commonwealth of Massachusetts. "Workers' Compensation Insurance Requirements." Accessed March 24, 2026.